|

As health and economic events continue to evolve at a brisk pace we are adapting our business practices to better keep our employees and clients safe, accommodate school closures, etc., while continuing to operate at a level required by you and these fast moving markets.

Beginning today, we will transition to remote work with a system in place to collect and process incoming mail and to transfer incoming calls out to the team. We all have access to our Cairn systems, and can trade, move money, access files, and otherwise serve your needs. During this unprecedented time, we will not be holding in-office meetings unless circumstances are exceptional. Hoping that you and yours remain well. The Cairn Team I wish that I could reach out and have a solid ten minute conversation with each and every investor with their money entrusted to Cairn. Unable to do that effectively, you deserve a few thoughts from us directly to supplement what you’re reading or hearing in the news.

Suddenly, things seem very different with the NBA suspending the season, travel from Europe restricted, and Tom Hanks infected and quarantined. In my prior message I put forward the idea that our collective reactions to the Coronavirus could have a large impact on the economy and our investments, and we took action to sell some long held positions in preparation. So now here we are. At this point stocks are no longer being bought and sold on fundamentals, and the prices we’re seeing are the result of massive liquidations based on fear. We’ve seen this movie before, with the current twist being that we can more clearly see what is driving the panic. While there are firms facing an existential threat, like the cruise lines and some smaller shale oil producers, a majority of the companies that we own are able to handle weeks or even months long disruptions to the free movement of people and goods, and will eventually move on from here. I do not like the prices being offered for our companies right now and I’m very reluctant to sell into this environment unless funds are needed immediately. There are some companies we are wanting to shed, but not on a day that smells of panic like today. We do also have our eye on some stocks that we may wish to buy at a newly reduced price. Looking forward, I believe that the federal government has a huge role to play in protecting our economy and our health. That role may be to provide some kind of relief to debt laden oil producers and transportation companies, payroll stimulus, or even providing temporary liquidity to financial markets. Unlike any crisis that we’ve seen in my lifetime, this one seems to have an expiration date as the virus works through its process and modern medicine eventually puts and end to the spread within the next year. The oil price war could end soon and suddenly with a few phone calls, or our government could take steps to protect our domestic energy production to combat the actions of “State Players” overseas. Regarding Cairn’s preparations for possible transit restrictions or a personal illness, we are able to access all of our trading and information systems remotely, and if need be can redirect our incoming calls to any phone that we wish. I hope it does not come to that, but it’s good to be prepared. The best course today is to look after our own health and that of those we’re responsible for and let this run its course. We’ll continue to look for opportunities to adjust our holdings as it makes sense. Regards, The Cairn Team Hi everyone,

This was quite a week in financial markets, so I wanted to add some color to Tim’s message from earlier in the week. Though we continue to have limited information on the Coronavirus, there no doubt will be an impact on business activity, consumer behavior, and investor psychology. Economic and market effects aside, we truly hope that containment and detection efforts continue to strengthen so more lives are not affected. Based on short-term market sentiment, over the last two weeks, the stock market went from being extremely complacent to pessimistic. On a short-term basis the market is very oversold. That does not mean it can’t get more oversold, but a short-term bounce could be likely. Our actions will be driven by what the data tells us, not by emotion. We will continue to sell or trim companies that exhibit high valuations, declining price momentum, and underwhelming fundamentals. We are also ready to purchase companies that offer the opposite and this recent sell off will help to provide some opportunities. As always, risk management is high on our priority list, but we must remain open to taking advantage of opportunities that present themselves. Enjoy the weekend and let us know if you have any questions or concerns. Best regards, Patrick & The Cairn Team Greetings,

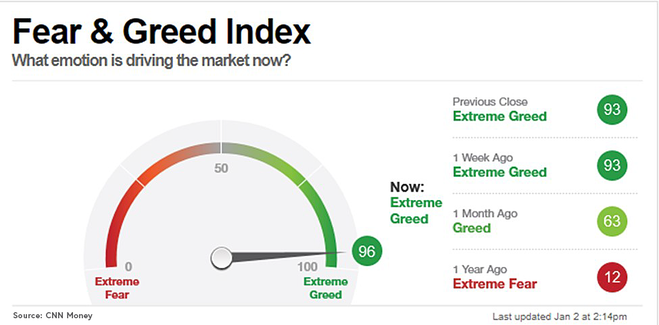

Unless you’ve been sequestered as a juror or have otherwise been off the grid, it’s likely you’ve heard that the coronavirus, or more accurately the various responses to the virus, have been impacting the global economy and hence the prices of your investments. It appears more likely each passing day that this will become a global pandemic, but much like our own body’s immune system, our collective reactions may cause more harm than the disease itself. While there’s much to learn about this new virus, it looks like the fatality rate is about 2% overall, with healthy populations faring better. While every death is regrettable, this disease’s impact is likely fleeting, without permanent structural changes to societies, families, or workforces. For some time, we’ve been tracking the progress of the US and world economies and noted many signs that we are in a mature stage of the growth cycle, with every indication being that while some major economies (US & China) are still growing, the rate is slowing. This is normal and expected after the long recovery from the bottoms of 2009, but it’s been recently exacerbated by the tariff battles. The various, and mostly rational, responses to the spread of the coronavirus are hampering international trade and will further suppress growth around the world, possibly pushing more economies into recession. The US economy is on better footing than most with strong employment, a huge internal consumer market, and access to most other markets on the planet. It’s generally a nice place to live too. We’ll note though, that stocks are expensive, and a little healthy doubt about where things are headed may just be the catalyst to help them get cheaper. We’ve been preparing for this by reducing equity exposure, selling stocks we view as too expensive, buying more income producing positions, and applying strict valuation criteria in our buy decisions. Our focus on risk management will not spare us from all the whims of the market, but it should bring you some comfort that wherever things go from here, you’ll have a reasonable experience. I’ll add that the stock market has been quite robust, so much so that even after the selloff of the past few days the S&P 500 Index is within 6% of all-time highs, and at the price it was in early December. I welcome your comments and concerns, so please feel free to call, stop by, or reply to this message. Thank you for your continued trust. Your Cairn Team  Hart Mountain Oregon. Photo by: Tim Mosier Greetings from the Northwest! Those familiar words have been a hallmark of our quarterly newsletters for many years and are likely to remain our first words for years to come, gently easing our readers into whatever more serious topic that is bound to follow. Working shoulder to shoulder with Jim Parr over the better part of two decades, I’ve learned that people enjoy, and get comfort from, the familiar. When Jim and I founded Cairn “way back” in 2007 we made a sincere effort to create a place where our investors, our people, could feel at home; a place where they were known, valued and thought about on a regular basis. It’s my desire to continue on this same path, putting you above all other goals, and you should expect no less than this. Inevitably there will be change, but change intended only to improve our service, improve our investing and improve our overall effectiveness. If we can do this and have you, our investor, feel like nothing has changed, only improved, then we will have succeeded. We have a great team today, I think the strongest in our 12 years here. As Jim mentioned in a prior note, Patrick Mason will be joining the ownership this year, adding a comforting layer of assurance that our methods and our mission can continue seamlessly in support of your goals. Read his message that follows, take it to heart, understand the choices that we are faced with in this complex economic and political environment, and know that you are being well served. Jesyca and Patricia put a smile on my face every day when I observe and hear the way they deal with our investors’ needs, simple and complex. Of course, Lara continues to provide a solid backstop to everyone’s efforts, and Jim cheers us on from his new and slightly different perspective. In the next few weeks I’ll be announcing another exciting addition to our team, but more on that later! I’ll leave the serious stuff to Patrick this time around, but I do want to sincerely thank all of you for being a part of the Cairn family, and in particular those of you who give us honest feedback on your experience, as it only serves to make us better. It’s my goal to revitalize our communications in 2020 to see and talk with as many of you as I can. Between the changes here, the upcoming election, and inevitable twists of the economic cycle, we should have plenty to talk about. Patrick's PartEquities finished the year in a celebratory mood, with U.S. large cap and small cap stocks posting fourth quarter gains of over 9%. Developed international stocks and emerging market stocks also fared quite well, with gains of 7% and 12% respectively. Fixed income, which had been a strong performer earlier in the year, posted flat returns as interest rates moved higher on longer dated bonds. Global markets were strong in 2019 after coming under pressure the year before. Concerns about trade and economic growth were pushed aside as investors cheered the Federal Reserve’s change in interest rate policy last January. As you can see by the Fear & Greed Index chart below, the majority of investors have now embraced equity market risk with little thought of the actual risk being taken.  In fact, the 2019 S&P 500 performance can be attributed to roughly 4% earnings growth, 2% dividend yield, with the remaining 25% attributed to multiple expansion (P/E ratio moving higher). In other words, over 80% of the S&P 500 Index return was generated by investors’ willingness to pay more for many years of future earnings, in the present. I think that fits the definition of greed pretty well. When valuations are already stretched, paying an even higher premium for future earnings can open investors up to experience larger losses or underwhelming gains in the future. Even with the strong performance of 2019, it would only take an 11% drop in the S&P 500 to get prices back to where they were in January of 2018. As we noted last quarter, we continue to observe softness in the current economic expansion, combined with generally high equity valuations. However, the data does not point to imminent recession and there are still opportunities for us to invest wisely. We continue to look for fundamentally sound investments selling at attractive prices, while balancing both risk and reward. As famed investor and writer Howard Marks likes to say, “Move forward with caution.” We think that is pretty sound thinking in the later stages of this cycle. Another topic of discussion this year revolves around the Secure Act and IRA distribution changes that passed into law recently. There are some major changes taking place, and we find the following two will impact the greatest number of our investors. The first involves the age at which a person must start taking their required minimum distribution. The second discusses the new parameters for beneficiaries that inherit a retirement account.

Estate planning issues may arise from these changes. The primary one we see is the naming of a trust as a beneficiary of an IRA. Attorneys will occasionally recommend this so that the assets are still under control of a trust while allowing the stretch provision for the RMD. Under the new law, all assets in the inherited IRA have to be distributed by the 10th year. Since there is no annual withdrawal required, the new provision could cause a large taxable distribution to the beneficiaries of the trust in the 10th year. As we meet with you over the coming year, reviewing IRA beneficiary designations will be an action item. My last topic involves cash management within your portfolios. As interest rates have done a U-turn over the last 12 months, interest paid on cash and money market funds has continued to fall. To make sure we are earning the highest interest on your cash while we either construct a portfolio, or wait for a new opportunity, we have implemented new cash management tools. To efficiently manage your cash, we are using liquid and safe securities consisting of CDs, T-Bills, position traded money markets, and short-term Treasury Bond ETFs that earn a higher interest rate than cash. We don’t want a lot of idle dollars earning very little in this challenging environment, and feel it is our job to manage your cash as effectively as possible. Thank you for your continued trust and please drop me a line if you have any questions or additional topics you wish to discuss. As always, our doors are open, the coffee is hot, and the parking is free, so please make a point to visit when you can.

Happy New Year, Tim Mosier, Principal Cairn Investment Group, Inc.  Photo by: Sean O. There is no Frigate like a Book :: To take us Lands away Nor any Coursers like a Page :: Of prancing Poetry —Emily Dickinson Greetings from the Northwest. During past market cycles I had a chance to read company reports, newspapers, and periodicals. Visit with company executives and their business to business trading partners. Reflect on business and industry segments and then pin it all up on my “wall of worry” and look at it. The process was a little like adding a new chapter to an ongoing story each quarter. Everything must continue to evolve. Well, welcome to the crazy-fast times. It is not as common as it once was to read a book. The tales of far-off lands now arrive as fast as the next news cycle, which is terrifying. It’s hard to find time to reflect on the good or the generous and the joy of a poem. And why would we when we can be entertained and amazed at the silly, greedy, and stupid behavior of so many prancing world leaders? Let’s take a moment of our precious time and focus on the real monster in the room. Uncertainty. It has often been said that the “market” likes good news, dislikes bad news and absolutely hates uncertainty. We should add that investors don’t like volatility. Uncertainty creates volatility, which causes investors to become restless. Restless about what? Patrick has been doing some thought-provoking work looking into the comings and goings of recessions. Yes, I’ve said it. Recession. We will have them. Patrick’s work is helping shed light on the recession monster and what we should be doing now… or not. Patrick's PartEquity returns during the quarter were mixed, with large-cap U.S. stocks posting a slight gain of 1.7%, while small-cap U.S. stocks, international developed stocks, and emerging market stocks posted slight losses of -2.3%, -0.79%, -4.75% respectively. Volatility has started to pick back up again, as markets grapple with a combination of trade tensions, changes in monetary policy, and slowing global growth. During the year we spend a lot of time with our clients discussing what is going on in their lives, the ongoing management of their wealth, and how we view this ever-changing market environment. We learn a great deal from these discussions. Though the economy has been strong over the last few years, in recent months we have observed recessionary fears rising amongst the public and the folks we talk with. It’s easy to see why, as the news chatters regularly about when the next recession will happen. This has largely been driven by the consistent yield curve inversion. As of August 31, 2019, the New York Federal Reserve Bank’s Recession Probability Indicator, based on the yield curve, has moved to a 37% chance of recession within the next 12 months, up from 14.5% a year ago. In April, I wrote about the lag times after the yield curve inverts and the inconsistent message that an inversion sends (read about it here). However, there are more data points in recent months revealing that the economic recovery is showing signs of stalling. We take evidence as it comes and do not attempt to predict the likelihood of when the next recession will start. At this time, the data we analyze does not point to immediate recession. Where we have been focusing our efforts is in analyzing what the most likely market experience would be if we entered a recession in the near term. Our conclusions are as follows:

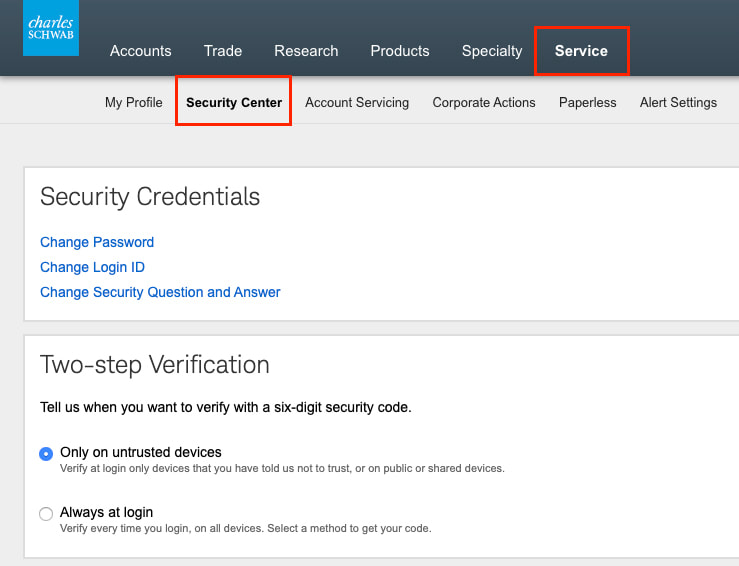

On a positive note, as Cairn searches the investment landscape for opportunities, we have continued to find quality companies to invest in that are trading at appropriate prices. Jesyca's PartAs our reliance on technology continues to advance, cybersecurity is of the utmost importance. We are always keeping an eye out for suspicious activity in your accounts and will call to verify as soon as we see any changes made. Cairn has your back. If you access your accounts online through Schwab Alliance, here are a few helpful tips to improve the security of your accounts:

Thank you, Patrick and Jesyca.

Come on by and let’s review your equity exposure and/or two-factor authorization. We’ll make sure the coffee is fresh. Happy Trails, Jim Parr, Principal Cairn Investment Group, Inc. 8/2/2019 :: Ticker: FL :: Div. Yield: 3.50% :: Closing Price: $39.36COMPANY DESCRIPTIONHeadquartered in New York, NY, Foot Locker is a leading operator of retail apparel and athletic footwear stores. The company offers merchandise under the names of Foot Locker, Lady Foot Locker, Champs Sports, Footaction, Kids Foot Locker, Runners Point, and Sidestep. Dick Johnson, who joined the company in 2003, is the CEO and Chairman of the Board. COMPANY HIGHLIGHTS AND FINANCIALSFounded in 1974, Foot Locker is a leading global athletic retailer operating approximately 3,200 stores in 27 countries. Unlike their competitors, Foot Locker focuses on high end sneakers and athletic footwear with a higher profit margin. Their company strategy is to generate long-term growth by empowering youth culture across communities. They demonstrated this with the opening of their Detroit store where they teamed with local artists, musicians, and athletes on store decoration, design concepts, and apparel offerings geared towards greater community and local youth connection. Over the next four years, Foot Locker is planning to aggressively invest in mobile and digital interaction technology to improve their adjustability to core customer shopping patterns. They will also revise merchandising and sales strategies with their main suppliers (e.g., Nike and Adidas). For example, in their newest New York City store in Washington Heights, Foot Locker customers can download the NikePlus app for product information and shoe availability—the first time Nike has made available their shopping technology to a third-party store. Customers can also use the Foot Locker app directly to shop for apparel and shoes across all brand offerings, and reserve forthcoming shoes prior to their in-store launch. Simultaneously, Foot Locker is shrinking their mall footprint from 80% to 70% of physical stores and increasing their standalone ‘power store’ format. These larger store concepts include design features and apparel offerings that reflect local communities and support the more interactive shopping experience. They include expansion across Asia, where the sneaker culture continues to gain popularity. In 2018 they opened a new power store in Hong Kong, and added digital platforms by partnering with Alibaba’s Tmall.com, which sells to Chinese consumers. These growth initiatives set the company up to deliver strong returns on capital, consistent profits, and dividend growth for shareholders in the coming years. KEY POINTS

VALUATION AND RISKSFoot Locker is trading at very attractive valuation levels. At their current sales and cash flow multiples, they are trading at roughly a 20% discount compared to their historical operating performance. Investor concerns over changing consumer shopping behavior surrounding physical mall locations are putting pressure on their shares. We realize that consumer shopping behavior is changing. Based on our analysis, we feel the market is overly pessimistic regarding the future of Foot Locker. If our analysis is incorrect, we believe there is a large margin of safety built into their current price. Risks we will monitor going forward include the company’s transformation from a traditional brick-and-mortal footprint to a digital one promoting local community experience, and Foot Locker’s relationship with their suppliers (e.g., Nike). Weighing both potential rewards and risks, we are optimistic that Foot Locker is a good long-term investment.

Cairn Investment Group and its affiliates (“Cairn”) produces Company Spotlight reports (“Reports”) for its clients and the general public. The Reports are impersonal and do not provide individualized advice or recommendations for any specific investor or portfolio. Investing involves substantial risk. Cairn makes no guarantee or other promise as to any results that may be obtained from using the Reports. Past performance should not be considered indicative of future performance. No reader should make any investment decision without first conducting his or her own research and due diligence. At various times Cairn may own, buy or sell the securities discussed for purposes of investment or trading. Cairn disclaims any and all liability in the event any information, commentary, analysis, opinions, advice and/or recommendations in the Reports prove to be inaccurate, incomplete or unreliable or result in any investment or other losses.

The Reports commentary, analysis, opinions, advice and recommendations represent the then current views of Cairn, and are subject to change at any time. The information provided in the Reports is obtained from sources the author believes to be reliable. However, the author has not independently verified or otherwise investigated all such information. This is not a solicitation or offer to buy or sell any securities. Cairn does not receive any compensation from any of the companies featured in the Reports. Any redistribution of the Reports or the information contained therein, without the written consent of Cairn is strictly prohibited.  Pine Forest Range, Nevada. Photo by: Tim M. Greetings from the Northwest. Our second quarter report is always a little chaotic to produce, since the Fourth of July holiday generally jumps right into the middle of the progress. The distraction of summer, and all that this Fourth brings with it, can cause your diligent advisors to be found yearning for the sizzling BBQ burger or the thirst-quenching relief of an ice-cold beer. This Fourth of July holiday was marked by distinctly cool weather that made the 32nd Waterfront Blues Festival, held along the bank of the Willamette River, quite tolerable in the warming afternoons all 4 days. If the afternoons were filled with blues, the morning of Sunday was exploding with excitement as the U.S. women’s national team took the soccer World Cup for the fourth time!! Being distracted from the business world for a bit was a nice relief from the growing number of global economic woes filling the airwaves recently. The most significant topic of today may be the announcement that Deutsche Bank is retreating from its global expansion and laying off 18,000 people. Oops. Closer to home, in the American oil patch, things are slowing down as well. “Hoping for a gusher, driller came up short.” It’s a common refrain heard in so many words about many business ventures these days. There are so many situations in business now that are good, but not quite great:

I’m sounding like a deflated firework and Patrick is itching to report on the current economic trends, so over to Patrick while I go squeeze our lemons into lemonade. Patrick's PartThe second quarter witnessed investors tossing tariff risks and economic growth concerns aside to focus on the possibility of the Federal Reserve cutting interest rates in the coming months. After bouts of volatility during the 4th quarter of 2018 and again in May, large company U.S. stocks closed near an all-time high. During this time, investors have experienced quite a change in economic growth expectations and monetary policy implementation. Just one year ago, the U.S. Fed was forecasting 2019 GDP growth to be 2.4% and 2020 growth to be 2.4%. When they released their most recent projections on June 19, those figures dropped to 2.1% and 2.0%, respectively. Looking at corresponding interest rate projections, previous forecasts were calling for a rise in the fed funds rate (short term interest rates) to 3.4% in 2020. The current forecast is predicting that interest rates will fall to 2.1%. What a difference a year makes. This flip-flop in policy has been a large component of falling interest rates across the bond market (prices rise) and the tailwind we have witnessed for U.S. stocks in the short term. As Danielle DiMartino Booth, former Federal Reserve Bank of Dallas Advisor and founder of Quill Intelligence, recently said, “We are having a recession party” when describing how positively the stock market is reacting to much slower growth that could result in easier monetary policy. As the S&P 500 index (large company stocks) trades close to an all-time high, while small cap and international stocks do not, we like to check underneath the hood to see what is really driving these recent returns. One question I looked at recently was, “Are all stocks carrying their weight and rising together or are just a few winners saving the day?” Examining this allows us to determine the overall health of the equity market. The breadth of participation signals how broad or shallow a market rally can be, which we find useful during the late innings of a cycle. One of the ways we analyze this is to look at the return contribution of the top names of the S&P 500. Recently, I ran comparison of the return contribution of the top 4 (largest) companies during 2013 and the contribution of the top 4 companies over the last 12 months. For the majority of 2013, we witnessed a broad based contribution and participation from U.S. stocks across the board. Which makes it a good comparison point. Here is the story the data tells: 2013:

Last 12 months:

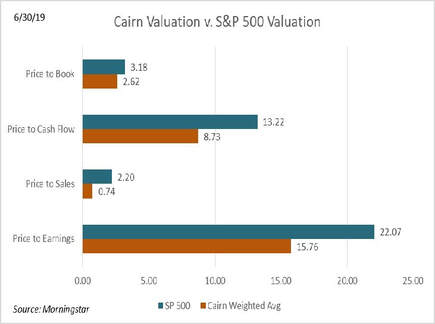

In essence, 2013 was a year where there was broad participation with many names of the index carrying the weight. Over the last 12 months you cannot say the same thing. A little more than 10% of the index is making up almost a quarter of the return. This indicates that the largest, and most popular, names have been carrying the load and the majority of companies have not been keeping up. I will leave it to you what you draw from this observation, but just a hint: It’s not sustainable in the long run. Cairn’s approach is not just following the crowd by investing more and more dollars into overly expensive companies. Our process of uncovering suitable investments is disciplined and consistent. As we stated in our September 2018 letter: “Through our quarterly letters and individual meetings we have discussed our process for uncovering successful investments, our current view of U.S. stocks, and how we are managing assets concurrent with that view. First, we are always on the lookout for industry leading companies that generate significant cash flows, with balance sheets that can provide financial flexibility. The final, and what we believe is the most important, piece is paying a price for a company that is significantly lower than what our analysis says the business is worth. We use a combination of cash flow analysis and the historical operating performance of the business to identify suitable investments, avoiding ones for which we would be paying too high a price, therefore limiting appreciation potential.” As the chart below illustrates, your portfolios trade at a significant discount to the S&P 500 by many different valuation metrics.  Lastly, here is just a small subset of the companies we own across portfolios we manage. We thought it would be of interest.

As we head toward the second half of the year, we will continue to look for opportunities, realizing that risk management remains paramount as we reach the late stage of both this economic and market cycle. If you’re interested in reading more about individual companies that we’ve researched, check out the Company Spotlights or give us a call and Jim, Tim or I will be happy to provide more information. Thank you, Patrick. As I’m fond of saying at the close of our quarterly letters, swing on by for a cup-o-joe. The coffee pot is always on. I’d like to add a personal note to all, about how thrilling it is to see our children grow. This event found me walking daughter Lindsey down the outdoor aisle in Wyoming as she accepted Aaron’s hand. Happy Trails, Jim Parr, Principal Cairn Investment Group, Inc.  Lindsey & Aaron. Best Wishes, Dad. 6/7/2019 :: Ticker: CTSH :: Div. Yield: 1.27% :: Closing Price: $62.78COMPANY DESCRIPTIONCognizant Technology Solutions, a global IT services company, partners with clients worldwide to provide technology solutions to transform and modernize digital needs. Headquartered in Teaneck, NJ, Cognizant operates under four segments: financial services; healthcare; products and resources (retail, manufacturing, travel, energy); and communications, media, and technology. Cognizant’s new CEO, Brian Humphries, recently joined the company from Vodafone Business, where he also served as CEO. COMPANY HIGHLIGHTS AND FINANCIALSCognizant Technology Solutions focuses on transforming the current and ongoing digital needs of their clients. Their global consulting team works closely with clients to develop digital platforms and solutions to increase operational efficiencies, while securing and modernizing their businesses. Due to the integrated nature of their IT work, Cognizant rapidly becomes engrained in client operations, making the costs of switching to a competitor high, and facilitating enduring client relationships. Over the last five years, Cognizant led the industry in revenue growth, averaging over 12% compared to single digit growth for primary competitors Accenture and Infosys. This high growth combined with solid client relationships expedited their becoming a large player in the global IT services and consulting arena. KEY POINTS

VALUATION AND RISKSCognizant Technology Solutions is trading at a large discount compared to their historical operating performance. Investor concerns over the recent CEO leadership change, and slower near-term growth in their two largest segments (financial services and healthcare), weighed on shares. We feel this is a short-term issue and presents an opportunity as the company has proven to operate at a high level, producing consistent growth over the long-term. Even with modest growth assumptions over the next business cycle, the company is trading at roughly a 20% discount to our fair value calculation. If our assumptions are incorrect, we believe this provides a margin of safety. Risks that we will monitor going forward include growth in the overall IT consulting market, and Cognizant’s current upper management transition. Weighing both potential rewards and risks, we are optimistic that Cognizant is a good long-term investment.

Cairn Investment Group and its affiliates (“Cairn”) produces Company Spotlight reports (“Reports”) for its clients and the general public. The Reports are impersonal and do not provide individualized advice or recommendations for any specific investor or portfolio. Investing involves substantial risk. Cairn makes no guarantee or other promise as to any results that may be obtained from using the Reports. Past performance should not be considered indicative of future performance. No reader should make any investment decision without first conducting his or her own research and due diligence. At various times Cairn may own, buy or sell the securities discussed for purposes of investment or trading. Cairn disclaims any and all liability in the event any information, commentary, analysis, opinions, advice and/or recommendations in the Reports prove to be inaccurate, incomplete or unreliable or result in any investment or other losses.

The Reports commentary, analysis, opinions, advice and recommendations represent the then current views of Cairn, and are subject to change at any time. The information provided in the Reports is obtained from sources the author believes to be reliable. However, the author has not independently verified or otherwise investigated all such information. This is not a solicitation or offer to buy or sell any securities. Cairn does not receive any compensation from any of the companies featured in the Reports. Any redistribution of the Reports or the information contained therein, without the written consent of Cairn is strictly prohibited. 5/23/2019 :: Ticker: BIIB :: Div. Yield: 0.00% :: Closing Price: $229.11COMPANY DESCRIPTIONHeadquartered in Cambridge, MA, Biogen is a biopharmaceutical company that specializes in the discovery and development of drugs for people suffering from neurological and autoimmune diseases. Their core business is a portfolio of medicines to treat multiple sclerosis (MS) and spinal muscular atrophy. Their CEO since 2017, Michel Vounatsos, was previously with Merck for 20 years. COMPANY HIGHLIGHTS AND FINANCIALSAccording to NeurologyToday, neurological diseases are the leading cause of disability worldwide. Founded in 1978, Biogen rapidly became a global leader in developing medicines to treat serious neurological diseases. They have the largest portfolio of treatment options for MS, and an estimated 35% of MS patients globally use Biogen medicines. Their core MS medicine business coupled with continuous development of drugs for other neurological diseases including dementia provides them with robust growth potential moving forward. Within the next few years, the company intends to expand their neurological portfolio to better address neuromuscular diseases, strokes, and movement disorders. Biogen’s disciplined capital allocation framework and high research and development spending (19% of revenue) provides the potential for consistent growth. KEY POINTS

VALUATION AND RISKSBiogen is trading at a large discount compared to their historical operating performance. Investor concerns caused the price move in March of 2019 after the company abandoned a late stage Alzheimer’s drug. While disappointing, and given the current price, we feel we are buying their still-expanding core MS business for free, and benefitting from future growth potential on their remaining portfolio. Even with modest growth assumptions over the next business cycle, the company is trading at a 20-30% discount to fair value. If our assumptions turn out to be incorrect, we believe this provides a margin of safety. Risks that we intend to monitor going forward involve regulation of drug prices and pipeline development. Weighing both potential rewards and risks, we are optimistic that Biogen is a good long-term investment.

Cairn Investment Group and its affiliates (“Cairn”) produces Company Spotlight reports (“Reports”) for its clients and the general public. The Reports are impersonal and do not provide individualized advice or recommendations for any specific investor or portfolio. Investing involves substantial risk. Cairn makes no guarantee or other promise as to any results that may be obtained from using the Reports. Past performance should not be considered indicative of future performance. No reader should make any investment decision without first conducting his or her own research and due diligence. At various times Cairn may own, buy or sell the securities discussed for purposes of investment or trading. Cairn disclaims any and all liability in the event any information, commentary, analysis, opinions, advice and/or recommendations in the Reports prove to be inaccurate, incomplete or unreliable or result in any investment or other losses.

The Reports commentary, analysis, opinions, advice and recommendations represent the then current views of Cairn, and are subject to change at any time. The information provided in the Reports is obtained from sources the author believes to be reliable. However, the author has not independently verified or otherwise investigated all such information. This is not a solicitation or offer to buy or sell any securities. Cairn does not receive any compensation from any of the companies featured in the Reports. Any redistribution of the Reports or the information contained therein, without the written consent of Cairn is strictly prohibited. |

RSS Feed

RSS Feed