|

Greetings from the Northwest. The essence of these reports from Cairn to you, our investors, should be primarily focused on you, the investment results and some sort of a gaze into the future, and thinking about how that future might affect the way we handle our investments. This time I’m going to start with a more personal note. Lara and I had a chance to meet up with our son, Tygh, who is an exchange student from OSU Forestry Engineering Program to the École Supérieure Du Bois in Nantes, France, focusing on International Timber Trade. Well, that’s a tongue twister of a sentence. We had a wonderful opportunity to spend Christmas and the New Year abroad. It was an unusual time to be out of the office as we went from one year to the next. Especially when there was so much news about potential, and eventually real, tax law changes. Patrick is going to pick up most of the load, describing some of these changes for us. Tim is going to update us on the phenomenon known as Bitcoin. And in general we’re going to be focusing on some of the things that we find particularly important at Cairn to keep all of our investment energy going in the correct direction. Our trip involved mostly France, although we had a wonderful few days in Iceland on the way over, and a few days in Amsterdam on the way back. We focused on a couple of locations with longer stays on the Brittany Coast and in Paris, renting an apartment in both places and doing most of the meal prep and grocery shopping ourselves. We had an opportunity to sort of sink into and enjoy France. The overarching condition that must be communicated to our investors is that there is a tremendous amount of economic horsepower happening in Europe. It is busy. Even in the winter there are lots of people spending lots of money. Loads of construction plus many products being invented and manufactured. They are absolutely determined to create new and interesting results in the way of transportation, education, banking, and healthcare. Over the last couple of years our investments have shifted to more exposure in European companies than in the past. I am extremely pleased to be in that situation, especially since it helps us move toward companies that are comparatively less expensive than some of their counterparts in the USA. Thank you for putting up with the anecdotal research that we carried out whilst being consumers in a foreign land. It is the place to be and we should look forward to enjoying international investing results.

Only one of these tasks was accomplished (barely), yet the equity markets marched to all-time highs. US stocks, measured by the S&P 500, returned 21.83% with international markets faring a bit better. We feel two acronyms can describe why investor euphoria continued in 2017 despite high valuations and continued geopolitical concerns: FOMO — “Fear of Missing Out” and TINA — “There is No Alternative.” Record low bond yields and paltry interest rates on safe haven investments have caused investors to reach for yield, raising already high risky assets, due to their fear of missing out and lack of an alternative to earn a satisfactory return. TINA can explain the most recent American Association of Individual Investors (AAII) poll where household allocation to stocks reached over 68%. This high allocation to stocks has not occurred since the late ‘90s, so clearly investors are feeling the need to reach for risk as fixed income and cash rates remain low. In our view, FOMO is the reason that many companies with little to no profits and high cash burns (Tesla and Netflix come to mind) trade at current prices. Other reasons given by financial pundits and talking heads on TV for the continued rise in equity prices are mostly noise and do not hold much water when analyzing the data. Ignoring the noise, FOMO and TINA, while sticking to our disciplined process, allow us to find ideas and investments that still offer attractive risk/reward traits. The silver lining is that not all companies are treated equally by investor euphoria, so we are still able to sift through the investment landscape and find bargains that the investment public has ignored. As an example, throughout the year we were focused on companies that had effective high tax rates that could benefit from tax reform. Many of these companies meeting that criteria are being cast aside over what we believe are excessive worries of competition and market share erosion. We are pleased with how our portfolios have done in spite of our conservative bias, as we continue to view the US market as expensive. We will continue to be vigilant in finding opportunities without losing sight of the fact that risks are higher than normal and preservation of capital is of equal importance while this nine year bull market matures. During the last week of December a new tax law was signed by the President. While there are many changes that are still being analyzed by tax experts, we want to touch on a few that we find meaningful.

Again, these are just some of the changes that were signed into law. For any detailed questions on how the new tax law affects you, your professional tax preparer will have the answers. I’m going to pass it over to Tim so he can talk about something much more exciting: BITCOIN! Enjoy. Tim's PartBitcoin? Lately we’ve had a number of our investors ask about Bitcoin (big sigh). It seems to be in the news daily, whether it’s up, down or both. While there are many sources that can provide a deeper plunge into the inner workings of Crypto-currencies and Block Chain Technology, we’ll take a moment and give our perspective on this phenomenon. Bitcoin as a currency — Not so much The reason it was created was to provide a secure and cheaply transferred currency useful to people and businesses worldwide. Despite its promise as a medium of exchange free from central banks and banking industry controls, it is not currently viable as currency for the ordinary human. Some reasons for this: Bitcoin is treated as any transaction that involves Bitcoin a tax may be due. Just as selling appreciated stock to buy a car will result in a 1099 for the capital gains, a “sale” of Bitcoin occurs during the conversion to dollars to facilitate the purchase of goods or services, which could result in a taxable event. Imagine getting a 1099 for the purchase of a sandwich! This is of course not happening, but it’s one of the novel effects that will need to be dealt with. In relation to the US dollar and other currencies, the value of Bitcoin is extremely volatile. Until prices of goods and services are quoted in Bitcoin across the globe, a conversion to traditional currency (i.e., US$, Euro, etc.) must happen in order to finalize transactions. This makes it unlikely that Bitcoin will be appropriate for widespread public use any time soon. Another issue for Bitcoin is that “depository” accounts used to hold it have been frequent targets for cyber theft; in some cases entire brokerage firms have been emptied of their Bitcoin. Normal monetary controls, developed over decades of experience, do not yet exist with Bitcoin; a fundamental benefit to some is a fundamental risk to others (think bearer bonds). VISA just cancelled a pilot program of Crypto-currency payment cards for some of these very reasons. Bitcoin as an investment — Hmmm In the sense that one can pay dollars for Bitcoin, and have more or fewer dollars at a future point in time, Bitcoin can be considered an investment, or at least has some features of investing. There is no way of measuring the value or potential value of Bitcoin in relation to the dollars one might invest, except by the market price at any given moment. There’s no productive enterprise being owned that may pay a dividend or rent, and otherwise have a widely agreed upon intrinsic value, as an investment in real estate, stocks or bonds would have. While Bitcoin holds promise for a future with a universal currency, it is unlike gold or other precious metals, which have held value to humans and governments for thousands of years and are unlikely to see this erode. Bitcoin and other Crypto-currencies are very new and it’s possible that they are but a transient experiment leading to something more permanent and useful in the future, in which case they will be worthless. We’ll see. If you decide to jump in Buy only what you can afford to lose! Enjoy the experience and learn from it. Don’t use the kids’ college fund!  As we go forward, and I have an opportunity to speak with you on the phone or in person, I’d be excited to give you a little more information on the places we explored abroad. Two adventures stick out as really remarkable: One was a fantastic storm on the Brittany Coast of France and then several days following, hiking the rocky, craggy, storm-ravaged coast line. Very, very beautiful and quite stimulating. Second, and without any particular planning, somehow we ended up at the top of the Eiffel Tower on Christmas Eve. That was a blast, absolutely gorgeous wonderful experience, chilly, people packed, fun. I look forward to seeing you throughout 2018, and until then…

Happy Trails, Jim Parr, Principal Cairn Investment Group, Inc. 11/17/2017 :: Ticker: OXY :: Div. Yield: 4.46% :: Closing Price: $68.40COMPANY DESCRIPTIONHeadquartered in Houston, TX, Occidental Petroleum is an international oil/gas exploration and production company with operations in the US, Latin America and the Middle East. The company operates three segments: oil/gas exploration, chemicals, and midstream/marketing. With the company for over 35 years, Vicki Hollub became CEO in 2016. COMPANY HIGHLIGHTS AND FINANCIALSOccidental Petroleum is the largest producer of oil in the Permian Basin (New Mexico and Texas). Since 2013 they have been reorganizing their asset base focusing on acquiring low cost, high return assets in the Permian Basin. This included spinning off their California oil/gas assets into a separate company, selling their non-core assets in the Middle East and North Dakota, further concentrating their effort in the lucrative Permian Basin. This strategy has strengthened the company’s profitability potential even if oil/gas markets come under pricing pressure. Occidental Petroleum also operates a chemicals segment, accounting for 35% of sales, manufacturing basic chemicals and vinyls.

VALUATION AND RISKSOccidental Petroleum is trading in line with their historical valuations and below fair value based on scenario analysis of free cash flow growth. Occidental has a dividend yield of 4.46% and generates over $1.3 billion in free cash flow, giving them the flexibility to continue to raise their dividend over time. The company forecasts their cash dividend will be raised if West Texas Intermediate (WTI) crude oil stays over $50 per barrel with the current dividend maintained at a WTI price above $40.00 per barrel. On a free cash flow basis, we expect the company to grow cash flow in the mid-single digits over the next decade, due to the company’s shift to higher margin assets. Modeling our conservative assumption places a price of $80 on the shares which is almost a 20% increase based on the share price as of the date of this report. If our conservative assumptions turn out to still be overly optimistic, we feel there is a margin of safety built into the current price based on the company’s strong cash flow generation and balance sheet. As we continue to monitor our investment in Occidental Petroleum, we would like to see continued discipline in regards to capital spending and their amount of leverage while continuing to grow their dividend. Continued focus on the company’s revenue breakdown and operating margins will be areas to monitor closely. Weighing the potential rewards and risks, we are optimistic that Occidental Petroleum will be a good long-term investment.

Cairn Investment Group and its affiliates (“Cairn”) produces Company Spotlight reports (“Reports”) for its clients and the general public. The Reports are impersonal and do not provide individualized advice or recommendations for any specific investor or portfolio. Investing involves substantial risk. Cairn makes no guarantee or other promise as to any results that may be obtained from using the Reports. Past performance should not be considered indicative of future performance. No reader should make any investment decision without first conducting his or her own research and due diligence. At various times Cairn may own, buy or sell the securities discussed for purposes of investment or trading. Cairn disclaims any and all liability in the event any information, commentary, analysis, opinions, advice and/or recommendations in the Reports prove to be inaccurate, incomplete or unreliable or result in any investment or other losses.

The Reports commentary, analysis, opinions, advice and recommendations represent the then current views of Cairn, and are subject to change at any time. The information provided in the Reports is obtained from sources the author believes to be reliable. However, the author has not independently verified or otherwise investigated all such information. This is not a solicitation or offer to buy or sell any securities. Cairn does not receive any compensation from any of the companies featured in the Reports. Any redistribution of the Reports or the information contained therein, without the written consent of Cairn is strictly prohibited. 10/9/2017 :: Ticker: COST :: Div. Yield: 1.29% :: Closing Price: $154.61COMPANY DESCRIPTIONHeadquartered in Issaquah, WA, Costco Corp. operates warehouse wholesale-membership stores. Through its stores it offers a variety of grocery products, clothing and other household goods. Craig Jelinek has been the CEO since 2012 and has been with Costco for over 20 years. COMPANY HIGHLIGHTS AND FINANCIALSCostco operates over 740 warehouses worldwide with over 200 stores outside the U.S. Costco offers over 90 million members a variety of household goods at low prices. According to Costco they are the 2nd largest retailer in the world with over $126 billion in sales for their 2017 fiscal year. Costco’s key strategy is to grow revenue through offering low prices on a number of bulk items. As an example, Costco sold $7.5 billion in meat and $1.6 billion in seafood during their 2017 fiscal year. Costco has a broad footprint across the U.S. with most warehouses located in larger populated suburban areas. With only 4% of sales currently via the internet, there is ample ability to expand their e-commerce business as more customers shift to an experience called “click and collect” in which they buy on line and then pick-up in the store. Costco has demonstrated consistent operating performance across many financial metrics. Though the grocery and retail business is fiercely competitive, Costco manages to generate high returns on capital (averaging over 13% during the last 5 years) and free cash flow generation. This allows the company to continue to invest in future growth initiatives (e-commerce and international expansion) while rewarding shareholders via an increasing dividend.

VALUATION AND RISKSCostco is trading at premium valuations compared to historical operating performance and peer group. As of the date of this report, Costco traded at over a 15% premium to its historical ten year sales multiple. Based on numerous free cash flow growth possibilities, we’ve assumed an overall compound annual growth rate (CAGR) in free cash flow of 7.0% over the long-term. This blended growth rate is well below the growth rate achieved historically. This reflects conservative assumptions based on increasing competition from new entrants into the market, such as Amazon, and pricing pressures from existing competitors like Walmart. Based on the probability of different growth rates for the company going forward, even our most optimistic outlook does not support the company’s current valuation, therefore caution is warranted. Costco is a well-managed, high quality company but with the increased risk of competition and the company’s elevated valuation we feel new investments in Costco should be deferred until valuations are more in line with the company’s operating performance.

Cairn Investment Group and its affiliates (“Cairn”) produces Company Spotlight reports (“Reports”) for its clients and the general public. The Reports are impersonal and do not provide individualized advice or recommendations for any specific investor or portfolio. Investing involves substantial risk. Cairn makes no guarantee or other promise as to any results that may be obtained from using the Reports. Past performance should not be considered indicative of future performance. No reader should make any investment decision without first conducting his or her own research and due diligence. At various times Cairn may own, buy or sell the securities discussed for purposes of investment or trading. Cairn disclaims any and all liability in the event any information, commentary, analysis, opinions, advice and/or recommendations in the Reports prove to be inaccurate, incomplete or unreliable or result in any investment or other losses.

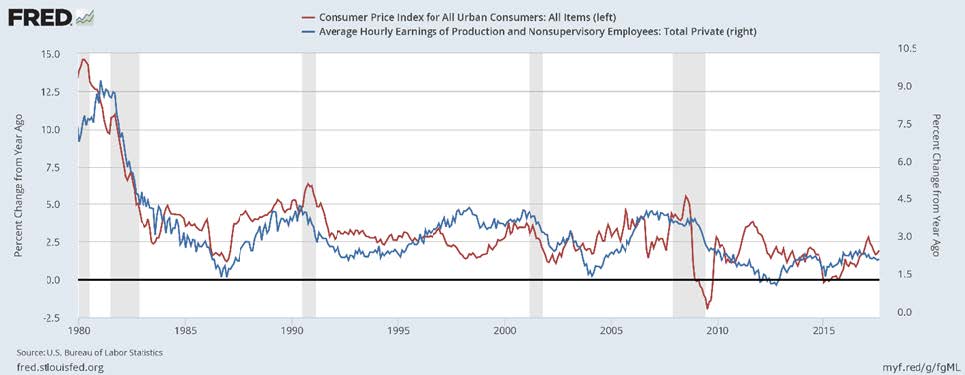

The Reports commentary, analysis, opinions, advice and recommendations represent the then current views of Cairn, and are subject to change at any time. The information provided in the Reports is obtained from sources the author believes to be reliable. However, the author has not independently verified or otherwise investigated all such information. This is not a solicitation or offer to buy or sell any securities. Cairn does not receive any compensation from any of the companies featured in the Reports. Any redistribution of the Reports or the information contained therein, without the written consent of Cairn is strictly prohibited. Greetings from the Northwest. Often I begin these letters reflecting upon those topics we have hanging on our wall of worry. It would appear, during this particular period of time, that the wall of worry is not that worrisome. At a very local level the recent forest fires that clouded our skies and challenged our transportation are diminishing. It’s wonderful to have some rain and it’s even better that we’ve been soaked with several inches of it. Over this last weekend, I took a trip up the Columbia River Gorge, traveling up the Washington side and coming down the Oregon side to see the extent of the Eagle Creek Fire. Yes, lots of terrible damage, but it really looks as if (like so many times before) the forest, the views, and the beauty will return. Instead of a wall of worry, we have a wall of a-lot-of-things-going-on. It’s a very exciting time at Cairn; many of you have been into the office over the last year and have experienced our new technology-bristling conference room and of course the espresso machine. In person and over the phone many of you have gotten to know Morgaine, who came to us not very long ago with a different kind of background, as a scholar of Ancient Mediterranean History, looking for a temporary job to rebuild her finances and head back to the Mediterranean and continue her education. Well, the time has come. Sadly for us, she is leaving. But, happily for us, Jesyca will be taking her place. Jesyca is a recent graduate of University of Colorado Boulder, and has moved to Portland to enjoy the vibe and the Northwest. She will be the person many of you will get to know on the phone or as you visit the office. Additionally, she will be helping Theresa with many of the tasks that happen in our office on a daily, weekly, monthly basis. Jesyca is one of the 110 new Portlanders who arrive each day to our fair city. Welcome to Portland, Jesyca! From a long list of important topics, there are several that are really worth focusing on this quarter. Number one, while we’re all interested and worried about the global economy, it has become clearer as the months roll by that the fear people had of debt after the recent “Great Recession” seems to be subsiding, and we are now becoming more comfortable with the increasing global debt. That’s typically not a good thing, but the expansion of our economy and economies globally seems to be taking it in stride. Number two, the Equifax security leak is a tremendous problem. We’ve taken a look at this and would encourage all of our readers to read the blog post Morgaine and Jesyca compiled on the current options to protect your personal private information. I believe it is important we all take this situation seriously and do everything we can to keep our personal data as safe as possible. The third topic that I’m confident will be fascinating to watch over the next months is the proposed changes to our tax laws. This could cause everybody to really think about the question: “What do you want your government to do for you?” And after you’ve made the list of what you want our Government to do, how do you finance it? So hang on and let’s get ready for some really interesting conversations about taxing ourselves so we can pay for what we want our Government to do. I’m going to pass this over to Patrick, and I think Theresa has an important message to deliver to us as well. I look forward to the next time we meet or speak and I look forward to a wonderful fall with a lot of delight in living in the Northwest.  Patrick's PartGlobal equities shook off a number of negative geopolitical headlines during the quarter. U.S. stocks rose 4.50%, while international stocks continued to outperform, rising 4.80%. Fixed income continued to defy the worry of rising interest rates as the U.S. 10 year Treasury yield remained at a low 2.32%. Economic growth around the world has shown better signs of life through the first 9 months of the year, which brings me to my topic for the quarter: Is the pick-up in GDP growth inflationary, and how will interest rates be affected? I’m not going to touch on the stock market, as our opinion has not changed from last quarter’s letter that U.S. indices, like the S&P 500, are becoming expensive. However, we continue to find value in individual companies, though not at the same level as a couple of years ago, so patience is warranted. Over the last 10 months the Fed has started the slow process of normalizing interest rates and reducing the size of their balance sheet. Since December 2016, there have been three 0.25% interest rate hikes. These increases have brought the fed funds rate to 1% - 1.25%. Historically, the Fed has raised interest rates in an attempt to cool down an overheating economy and to put the brakes on inflation. One indicator that we look at to take a reading on the health of the economy is the change in employee earnings versus inflation. The chart below shows the year-over-year change in inflation (red line, measured by CPI) and the year-over-year change in average hourly earnings for employees (blue line).  As you can see, historically there has been a very tight relationship between the two. Actually, year-over-year changes in average hourly earnings tend to lead changes in inflation. As the bottom right of this chart shows, the growth of average hourly earnings peaked in 2016 and has been steadily declining since. This is in contrast to the pick-up in inflation that has taken place since 2015. This matters when taking a look at Fed policy going forward and how future interest rate increases could affect the economy. If inflation is set to decline in line with what hourly earnings growth is telling us, then the Fed will have some very tough decisions about how quickly to raise interest rates going forward. Overall, the pick-up in GDP growth does not look to be inflationary at this point. If that is the case, monetary policy risks will remain high as the Fed will have to weigh continued normalization of interest rates against the risk of slowing down the economy. These are just some of the many data points we look at when thinking about your investment portfolios. Please email or call if you want to discuss any of these topics in more detail. Theresa's PartOften fall is a time to regroup and get organized. Maybe even catch up on some neglected chores. When you have a change of address, please contact me. I would like to coordinate the address change for you at both Cairn and the custodian. Not having a current address on file can cause information delays, and can eventually cause restrictions on your accounts. I will need your signature to change your address at the custodian. You may contact me directly via phone 503.241.4901 or email. Thank you Theresa. Please take me up on my standing offer to swing by for some local joe. The pot is always on. Happy Trails, Jim Parr, Principal Cairn Investment Group, Inc. P.S. Our website relaunch was a great success. The first 20 people responded to the challenge within two hours! Many more over the next several days! We sent coffee cards to all who responded, even after the first 20. I haven’t told Tim the grand total because it will bust the marketing budget. Thanks for participating.

Detect Check the status of your accounts (financial and credit history) Prevent

Plan

Check with Equifax to see if you were affected by the breach:

A. Placing a Security Freeze on Your Credit (Guidelines from Consumers Union): Deciding Whether to Place a Security Freeze How to Place a Security Freeze In order to effectively freeze access to your credit files, you must request a security freeze to be placed at each of the three major credit bureaus. Pricing is determined by state but paid to the respective agency. By Phone: Call each of the credit bureaus at the number provided below:

Online: On each credit bureau’s website (TransUnion, Equifax and Experian), you can find an online form to place your security freeze.  B. Initial Fraud Alert To set a fraud alert, contact just ONE of the credit card bureaus and ask for an initial fraud alert. Once the alert is set, it will last 90 days. After that, you'll have to renew it:

C. Purchasing Identity Theft Protection vs. DIY: While this article is promotional, it gives a very clear rundown of the difference between identity theft protection and credit monitoring. This article goes through many aspects to consider when deciding the next steps of action to take after this Equifax breach. 9/13/2017 :: Ticker: KR :: Div. Yield: 2.3% :: Closing Price: $21.73COMPANY DESCRIPTIONHeadquartered in Cincinnati, Ohio, Kroger Co. is the largest U.S. grocer. It operates multi-department stores, jewelry stores, and convenience stores throughout the United States. Kroger also offers its own private label that it produces from its 38 food production plants. William McMullen has been the CEO since 2014, spending over 37 years with Kroger. COMPANY HIGHLIGHTS AND FINANCIALSKroger operates, either directly or through its subsidiaries, approximately 2,800 supermarkets and multi-department stores, approximately 1,400 of which have fuel centers. Kroger operates under 21 banners that include Fred Meyer, QFC, Kroger, City Market, Dillons, Food 4 Less, Fry’s, Harris Teeter, Jay C, King Soopers, Ralphs, and Smith’s. Kroger also operates over 700 convenience stores, either directly or through franchisees. Kroger has an additional 319 fine jewelry stores, which alone account for $345 million in annual revenues, making it one of the largest fine jewelers in the U.S. Kroger is the fifth largest pharmacy operator in the U.S. by number of locations. It offers pharmacy services in over 2,200 of its stores, which accounts for close to 10% of its revenue. Kroger operates one of the broadest footprints in grocery with a vast majority of its supermarkets within 2-2.5 miles of its customers’ homes. Their size and scale puts them in an enviable position to compete through digital platforms for home delivery or curb side pick-up services. This is a key differentiator when comparing Kroger to competitors, and a big asset moving forward as the grocery business adapts to new competition. Kroger recently opened its newest store concept, “Fresh Eats MKT,” which is a combination convenience store, pharmacy, and gas station, focused on higher quality food offerings. Kroger has demonstrated consistent operating performance across many financial metrics. Though the grocery business is fiercely competitive, Kroger manages to generate high returns on capital (averaging over 12% during that last 5 years) and free cash flow generation. This allows the company to continue to invest in future growth initiatives (e-commerce and small store formats) while rewarding shareholders via an increasing dividend and timely share repurchases.

VALUATION AND RISKSKroger is trading at attractive valuations compared to historical operating performance and peer group. As of the date of this report, Kroger traded at over a 25% discount to its historical five year sales and cash flow multiples. Based on numerous free cash flow growth assumptions, we assume an overall compound annual growth rate (CAGR) in free cash flow of 4.5% over the long-term. This blended growth rate assumption is well below the growth rate achieved historically. This reflects conservative assumptions based on increasing competition from new entrants into the market (Amazon) and pricing pressures from existing competitors like Walmart and German-based Lidl. If our conservative estimates turn out to be overly optimistic, we feel there is a margin of safety built into the current price. These risk factors will be monitored, but at current valuations combined with the company’s financial strength, we feel the risks are represented in the current price and that future growth potential remains strong.

Cairn Investment Group and its affiliates (“Cairn”) produces Company Spotlight reports (“Reports”) for its clients and the general public. The Reports are impersonal and do not provide individualized advice or recommendations for any specific investor or portfolio. Investing involves substantial risk. Cairn makes no guarantee or other promise as to any results that may be obtained from using the Reports. Past performance should not be considered indicative of future performance. No reader should make any investment decision without first conducting his or her own research and due diligence. At various times Cairn may own, buy or sell the securities discussed for purposes of investment or trading. Cairn disclaims any and all liability in the event any information, commentary, analysis, opinions, advice and/or recommendations in the Reports prove to be inaccurate, incomplete or unreliable or result in any investment or other losses.

The Reports commentary, analysis, opinions, advice and recommendations represent the then current views of Cairn, and are subject to change at any time. The information provided in the Reports is obtained from sources the author believes to be reliable. However, the author has not independently verified or otherwise investigated all such information. This is not a solicitation or offer to buy or sell any securities. Cairn does not receive any compensation from any of the companies featured in the Reports. Any redistribution of the Reports or the information contained therein, without the written consent of Cairn is strictly prohibited. 8/2/2017 :: Ticker: SONC :: Div. Yield: 2.37% :: Closing Price: $23.78COMPANY DESCRIPTIONHeadquartered in Oklahoma City, OK, Sonic Corp. operates and franchises the largest chain of drive-in restaurants across the US. James Hudson is the CEO and has been with Sonic Corp. since 1984. COMPANY HIGHLIGHTS AND FINANCIALSFounded in 1953, Sonic Corp. now serves over 3 million customers daily across 45 states. Sonic has made its name serving fresh hamburgers, hotdogs, onion rings, and shakes via a drive-in, carhop service restaurant theme, averaging between 16 to 24 parking spaces that use an intercom ordering system. The restaurant boasts the ability to have over 1 million drink combinations. Combined with low prices, all fresh ingredients, and intelligent advertising, Sonic has been able to grow profits at attractive rates and maintain a loyal customer base. Sonic Corp. has a strong operating history. The company has over a decade of profitability, while producing operating margins of over 20%. Disciplined capital allocation has allowed them to produce returns on capital of over 21% in 2016.

VALUATION AND RISKSAs of the date of this report, Sonic Corp. is trading at a discount to its historical operating metrics and to its peers (McDonalds, Jack in the Box). We forecast Sonic Corp. will be able to grow cash flows in the low double digits going forward, which is more conservative than its historical growth rate of over 20%. With our conservative assumptions, we feel Sonic trades at a 30% discount to its fair value. If our conservative assumptions turn out to be too optimistic, we feel there is a margin of safety built into its share price. Sonic Corp’s primary risks are changing consumer tastes and health habits and increasing wage costs as more states implement higher minimum wages. Even when considering these negative potential impacts we feel Sonic Corp. is a good long-term investment.

Cairn Investment Group and its affiliates (“Cairn”) produces Company Spotlight reports (“Reports”) for its clients and the general public. The Reports are impersonal and do not provide individualized advice or recommendations for any specific investor or portfolio. Investing involves substantial risk. Cairn makes no guarantee or other promise as to any results that may be obtained from using the Reports. Past performance should not be considered indicative of future performance. No reader should make any investment decision without first conducting his or her own research and due diligence. At various times Cairn may own, buy or sell the securities discussed for purposes of investment or trading. Cairn disclaims any and all liability in the event any information, commentary, analysis, opinions, advice and/or recommendations in the Reports prove to be inaccurate, incomplete or unreliable or result in any investment or other losses.

The Reports commentary, analysis, opinions, advice and recommendations represent the then current views of Cairn, and are subject to change at any time. The information provided in the Reports is obtained from sources the author believes to be reliable. However, the author has not independently verified or otherwise investigated all such information. This is not a solicitation or offer to buy or sell any securities. Cairn does not receive any compensation from any of the companies featured in the Reports. Any redistribution of the Reports or the information contained therein, without the written consent of Cairn is strictly prohibited.

Greetings from the Northwest. It’s the July 4th weekend and I’m not where I thought I was going to be. A couple of weeks ago I was having a conversation with a fellow who mentioned he knew someone who had a tractor for sale in Spokane, WA. My wife’s family has a filbert orchard and a tractor can be a darn handy tool. Especially if it’s a lightly used, well cared for, 12 year old tractor. So here I am piloting my pickup and trailer through the Columbia River Gorge and central Washington desert. I was enjoying an ice cold Starbucks coffee when I zipped right past the State of Washington’s first commercial hemp growing operation outside of Moses Lake. Commerce is flowering in the Columbia Basin. The person I’m going to see about the tractor lives a little north of Spokane, which is nearly a 350 mile drive one way. And it’s hot. I’ve always enjoyed Spokane; over the years it’s been such a hotbed of economic activity, mining, banking, logging, farming, technology and recreation. In general it is a really interesting area to recreate in as well as to have a business. So after many hours, I pulled into a wonderful family’s farm, and after serious negotiations I loaded and hauled a new used tractor back to the Willamette Valley. These kinds of trips typically stretch a little longer because I like to meander and see interesting things along the way. I deviated from the highway route near the Tri-Cities of Pasco, Kennewick and Richland. With a pelican as my guide, I crossed over the Columbia River on the recognizable cable bridge, officially named the Ed Hendler Bridge, into downtown Kennewick.  Ed Hendler Bridge, Kennewick, WA. Photo by: Lara P Ed Hendler Bridge, Kennewick, WA. Photo by: Lara P The Fourth of July also brings an extraordinary event to Portland each year, The Blues Festival. Being there in person is of course fantastic, but this particular weekend I’ll take my jazz by radio. I always enjoy hearing Booker T play “Green Onions” and many others. The Blues Festival celebrated its 30th anniversary, and while it’s possible more Portlanders know about 30 years with the blues, we won’t forget that this is also Cairn Investment Group’s 10th anniversary. Tim and I and our team have been extraordinarily pleased to be connected to the wonderful group of investors who make up Cairn Investment Group. Over the last ten years Cairn has evolved considerably. It is exciting to see the growth in our research capacity, allowing us to dive even deeper into the valuations of our investments. Patrick will be covering the details of projects we’ve been working on the last few months. Tim is going to cover some of the components of our relationship with you. Patrick's PartThe broader markets continued their positive momentum during the second quarter, with US stocks rising over 3% and international stocks faring a bit better, rising over 5%. When you look underneath the hood that drove returns in large cap US stocks, the companies that have been carrying the load (Apple, Amazon, Facebook, Google) started to lose some of their luster, all suffering negative returns during the month of June. This has started to benefit active management and value-conscious strategies, as many of the names that have been carrying the broader market have risen to price levels that we consider to be far above fair value. This brings me to my topic for this quarter: Where are valuations for the broad market? And how does our approach differ from simply investing in indices? Many clients have voiced concern over the last year that they feel markets are “expensive” and are mostly wanting a return “of” capital more than a return “on” capital. We manage all our clients’ wealth with a “return of capital” being the building block of our philosophy while achieving a reasonable “return on capital.” We share the view with these clients that the broad US markets are above fair value. Below is a chart that maps the total market cap of US stocks measured against US GDP. This is the so-called “Buffet Indicator” and, as you can see, it has risen to historically high levels. We have talked in the past about the potential risks of index investing in the US, and this indicator shows some of the risks going forward in blindly investing in indices that are potentially filled with overvalued stocks.  Source: www.gurufocus.com Our philosophy is built around constructing equities portfolios that demonstrate high quality companies at attractive prices, and then being patient while our thesis plays out. We continue to find attractive long term investments even as US markets reach historic highs. We have found some opportunities in the health care and consumer markets. We feel that the markets have unfairly priced-in many negative events that probably won’t happen (i.e. the Amazon taking over the world effect). For patient, research-oriented investors, like ourselves, this creates opportunities to invest in well managed companies at historically low valuations. As Jim has said many times in the past, “We do not own the stock market.” Not owning the whole stock market when valuations are at high levels can do wonders to protect against loss when volatility rears its head again. So while the markets might be expensive, rest assured: Our goal is that your portfolios are not. Thank you for your continued interest and, as always, feel free to reach out to me with any questions. Tim's PartWhen you began your relationship with Cairn, one of the processes that you went through with us was to fill out and discuss an Investor Profile; it’s a document that we use to learn about you, your goals, and your attitudes about money and investments. This document is important because it leads directly to the investment choices that we make on your behalf, so it makes sense that it be accurate and up to date. Much has changed in the world since we opened our doors ten years ago. We’ve been from economic boom to bust to a slow cooker boom again. We’ve seen three US Presidents, the advent of the iPhone, a significant re-mapping of the Portland food scene, and, of course, we’re all ten years older. If you feel that your circumstances have changed enough to warrant a reassessment of your profile, please let us know. We welcome a chance to revisit this and learn what’s new in your life. Come on by for a cup of hot or iced coffee when you have a moment. We’d like to show off the techniques we are applying.

Happy Trails, Jim Parr, Principal Cairn Investment Group, Inc. 6/28/2017 :: Ticker: GWW :: Div. Yield: 2.90% :: Closing Price: $176.96COMPANY DESCRIPTIONHeadquartered in Lake Forest, Illinois, W.W. Grainger is a global distributor of maintenance, repair and operating (MRO) equipment, supplies, and services. As a major supplier to the industrial sector, the company sells everything from gloves, safety equipment, AC units, to plumbing supplies. Its extensive product selection combined with its inventory management services has contributed to being a leader in the MRO market. Grainger serves roughly 3 million businesses and institutions worldwide via their network of distribution centers, websites, and branches. Donald Macpherson was appointed CEO in October 2016 and has been with Grainger since 2008. COMPANY HIGHLIGHTS AND FINANCIALSThe MRO market is highly fragmented but Grainger has separated itself from competitors by offering customized services and enhanced e-commerce platforms that cater to large customers. Approximately five thousand suppliers provide Grainger with more than 1.6 million products. Grainger maintains strong relationships with its active customers via enhanced inventory management solutions. It is estimated that Grainger controls 6% of the US market share in this space with its $10 billion in annual revenue. Through continued investments in e-commerce, Grainger has become the 11th largest website (by sales) in the US, which accounts for close to 50% of their revenues and 65% of their orders. Of the 250 branches that Grainger operates, the majority are company owned without mortgages, increasing balance sheet strength, and allowing for increased flexibility in their continued transition to digital platforms. The company’s operating performance has been very strong over time. The firm generates consistent operating margins, averaging 10% over the previous 10 years. They also generate much higher returns on capital than other logistics firms due to their low asset base and strong balance sheet (ROIC has averaged 18% over the last 10 years). This, combined with Grainger’s focus of returning cash to shareholders via dividends (45 consecutive years of dividend increases), and strategic buybacks, shows how focused and shareholder friendly the management team has been over time. With low debt and strong cash flow generation, this should allow Grainger to continue to grow over time and allow it to do so without excess leverage.

VALUATION AND RISKSGrainger is trading at a discount compared with historical valuations and below fair value based on scenario analysis of free cash flow growth. Grainger has a dividend yield of 2.90% and generates significant free cash flow, creating the flexibility to continue to raise their dividend over time. We expect the company to grow free cash flow on average at 4.5% over the next decade, below its historical average, due to increased competition and pricing pressure from clients. Modeling our conservative assumption places a price of $200.00 on shares which is almost a 12% premium based on current price. If our conservative assumptions turn out to be overly optimistic, we still feel there is a margin of safety built into the current price based on the company’s high returns on capital, strong cash flow generation, and strong balance sheet. The largest risks we view is an overall cyclical downturn in the global economy and increased competition from larger more diversified firms. Though we believe that Grainger’s strong customer relationships, technology platform, and diversified revenue stream would allow the company to continue to earn high returns on capital, it could put short term pressure on operating performance.

Cairn Investment Group and its affiliates (“Cairn”) produces Company Spotlight reports (“Reports”) for its clients and the general public. The Reports are impersonal and do not provide individualized advice or recommendations for any specific investor or portfolio. Investing involves substantial risk. Cairn makes no guarantee or other promise as to any results that may be obtained from using the Reports. Past performance should not be considered indicative of future performance. No reader should make any investment decision without first conducting his or her own research and due diligence. At various times Cairn may own, buy or sell the securities discussed for purposes of investment or trading. Cairn disclaims any and all liability in the event any information, commentary, analysis, opinions, advice and/or recommendations in the Reports prove to be inaccurate, incomplete or unreliable or result in any investment or other losses.

The Reports commentary, analysis, opinions, advice and recommendations represent the then current views of Cairn, and are subject to change at any time. The information provided in the Reports is obtained from sources the author believes to be reliable. However, the author has not independently verified or otherwise investigated all such information. This is not a solicitation or offer to buy or sell any securities. Cairn does not receive any compensation from any of the companies featured in the Reports. Any redistribution of the Reports or the information contained therein, without the written consent of Cairn is strictly prohibited. |

RSS Feed

RSS Feed