|

Greetings from the Northwest. Was that a Mack Truck or a herd of reindeer that knocked us off our feet? I didn’t catch a glimpse of the perpetrator, but it sure was nice of him to pick us back up and dust off our coats before he left. I’m talking, of course, about last year. Done with that, let’s move on to better days, and I do believe that better days are ahead. On a global scale, private enterprise has figured out how to operate while hampered by the confusing regulations and ever-present risks. Consumers are consuming, homebuyers are buying, etc. People and companies everywhere have pulled forward their use of technology for communicating, shopping, and more, by several years; yet it seems like we all still want to visit Costco and Fred Meyer between our Zoom meetings. As the health crisis eases with the coming vaccines, we’ll find out just how much pent-up demand exists. My sense is that it’s high. When we get the green light, we’ll be eating out, shopping, and traveling in vast numbers. Continuing in a more positive vein, I am so impressed by the people iour community who have, throughout the crisis, kept on task, helping those in need, whether that be financially, emotionally, medically, or all the above. We’ve seen strong giving from our clients and can see the good this spreads in the community. Similarly, I’ve observed an unabated commitment to important environmental projects in our state and elsewhere, with people giving their time and money trying to make a positive impact. Thank you. There will be challenges; we’ll all learn the tax impacts of the election in coming months, and we’ll all adapt. The stock market itself has already celebrated some of this success, so its performance may not be so rosy. I’ll leave it to Patrick to explain our thoughts on that in more detail. Speaking of Patrick and a brighter future, I want you all to know that as of January 1, Patrick is officially on the ownership team at Cairn. This is an important step for him, for your relationship with Cairn, and our ongoing growth, health, and continuity. Welcome, Patrick!

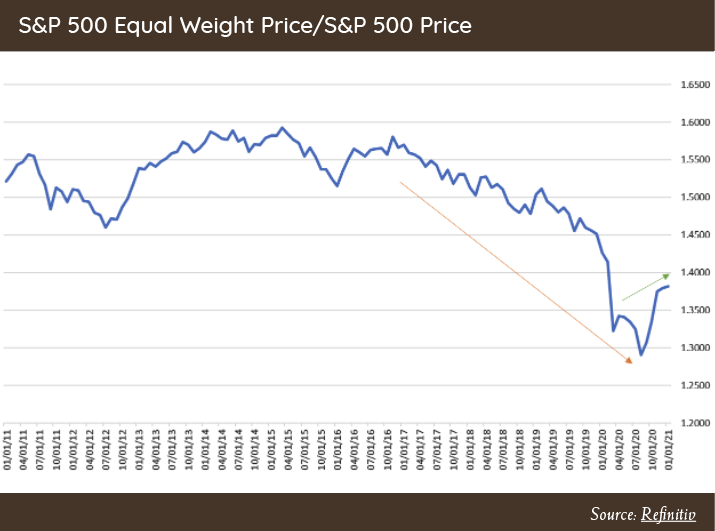

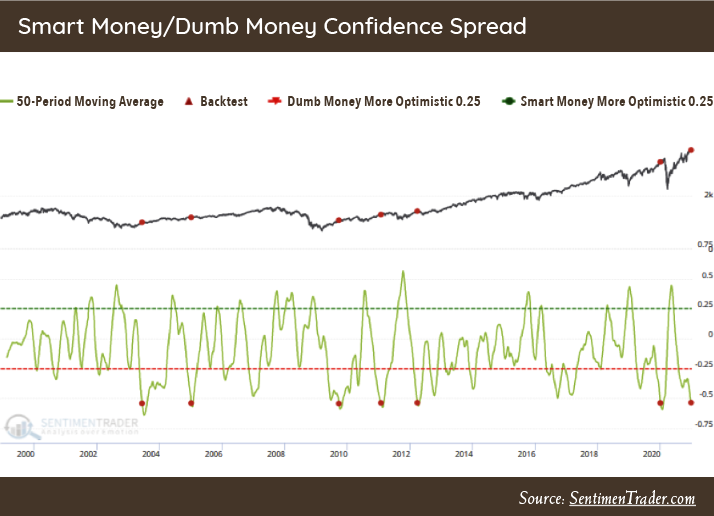

Patrick's PartEquities posted a strong finish to 2020 with most indices up low double digits for the quarter. Investors continued to focus primarily on positive vaccine news versus a still muddling economy with lofty equity valuations. Small-Cap stocks were the biggest winner, rising 31.37% during Q4, while bonds posted a modest 0.67% gain. During our Q3 letter and our mid-quarter update we discussed where we are finding opportunity based on the large mis-pricing in small cap and value stocks, and though the first quarter of the year did not meet our expectations, portfolios have benefited from the change in market participation we are currently witnessing. One of our favorite indicators to track market participation (breadth), is the S&P 500 Equal Weight Index over the S&P 500 Cap Weight Index. When this indicator is moving down, market participation is narrow and being driven by a few large companies (like FAANG stocks). When it is moving up, the smaller companies are carrying more of the load and participating in a meaningful way, which is the current trend as you can see in the chart below.  We have written quite a bit about high valuations and risk over the last few years. Though our concerns about valuation have not receded, observing more broad participation in the equity markets is a positive. With the rebound in equities that took place in April, we are now witnessing sentiment indicators at optimistic levels. One of our favorite sentiment indicators is the Smart Money vs. Dumb Money Spread released by our friends at SentimenTrader.com. This indicator measures money flows based on large option trading versus small speculative option trading. This is a contrarian indicator based on the logic that large institutional hedgers and participants have more knowledge and therefore are the “Smart Money.” As you can see from the chart below, when “Dumb Money” is at extremes, this tends to be a warning sign for the coming months.  We are witnessing a tale of two markets summarized by: better participation across asset classes, and companies that will benefit from further economic improvement. Countered by equity markets that exhibit excessive valuation and frothy sentiment dampening future return potential. We have positioned portfolios accordingly, to take advantage of markets that are rewarding attractively valued companies and asset classes, while maintaining some extra cash and fixed income to act as a ballast in case more turbulent times arrive. Thank you for your continued trust. I always enjoy conversations with clients regarding any of these notes or the data we analyze, so please drop me a line if you care to discuss in greater detail. Thanks, Patrick!

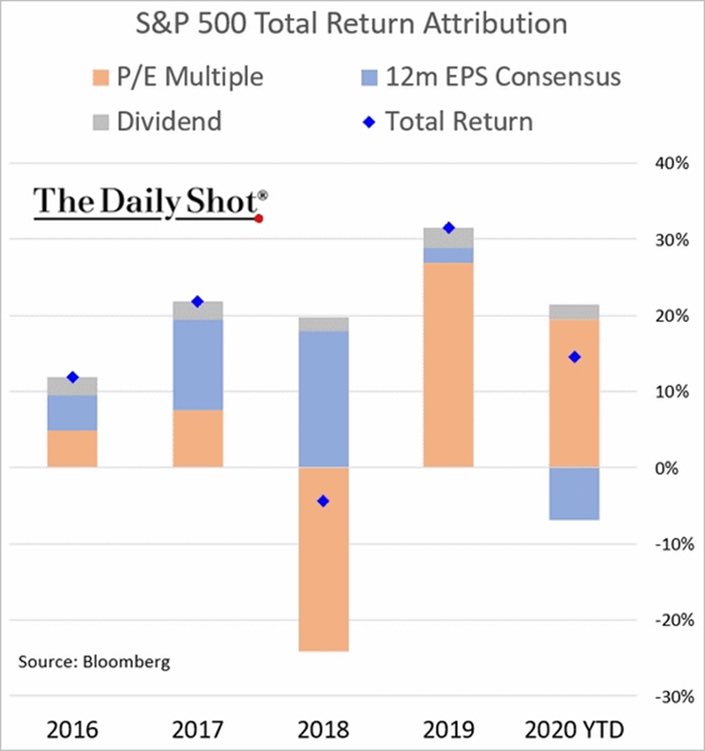

Here’s to a happier 2021. Tim Mosier, President Cairn Investment Group, Inc. A lot has happened since our last note! The virus is running rampant, but the election is behind us and multiple vaccines appear to be effective and on the way. The markets have interpreted the sum of these events to be positive and we’ve seen an amazing uptick in November, with broad participation across sectors, companies, and asset classes, lifting our account values. The shift of interest towards stocks that may benefit from a “re-opening” is notable and we own many of these. In our third quarter letter, we discussed the risks we are witnessing in large-cap technology stocks, the opportunities in small-cap stocks relative to large-cap stocks, and value versus growth stocks. In November it seems other market participants have started paying attention to the large valuation gaps of these two groups with small cap stocks having its third best relative performance month versus the S&P 500 in the last 20 years, and value stocks having their best absolute performance month in over 20 years. Although it is still too early to call this a permanent change in trend, it is encouraging to witness more broad participation across the market instead of only a handful of overly expensive companies producing the majority of returns. We are pleased with the recovery that markets have staged, but we cannot forget about the risks that are still present. We have written about valuations at length, and especially valuations surrounding large cap US stocks. With the recent run up, valuations for the S&P 500 stand at highs last witnessed in the year 2000 and right before the great depression. Economic activity and Company earnings, though improving, are still mired in recession from our battles with COVID-19, with company earnings showing a -6.3% decline from the previous year during the third quarter. Analysts estimate that earnings are not expected to reach their 2019 levels until the start of 2022. We know the market is a forward indicator but basing today's price on the hope of an earnings recovery in 2022 shows how much optimism is built into this equity market. As you can see from the chart below, the return of the S&P 500 to date, is comprised almost entirely by multiple expansion (investors paying more for an undetermined amount of future earnings). A risky proposition in our view.  Source: @lizannsonders We are very excited about the possibilities of vaccines being distributed as we start the new year. I think everyone is ready to get back to a more “normal” way of life, and many of our equity positions are being held at the right price to benefit from further recovery, or expectation of it. However, we must always remain focused on what is already reflected in current prices so that we can understand the risks and opportunities that the markets are presenting. The good news is we are still finding some opportunities. Walking this tightrope, we still hold extra cash and fixed income in the portfolios to protect against the market going through another bout of pessimism.

We hope you and your families have a safe and happy holiday season. Thank you for your continued trust and please reach out if you want to discuss any topic in greater detail. Your Cairn Team So, what happens to the markets on November 3rd? It’s likely to be noisy with the first moves being quite reactionary. Focusing too much on this event, even if the outcome is ugly, is not a great use of one’s time. Here are the things that we think will cause more substantial moves in the next several months: 1. StimulusThis may be the reason why anybody has a stock portfolio that’s not down significantly in 2020. Without it we’d be in a real mess. Most financial experts and politicians believe that another stimulus package is necessary for the nation to avoid a worsening financial and social crisis. This view is shared, through differing lenses, by both political parties, so I think we’ll have more stimulus. It’ll be bigger if the Democrats win the White House and the Senate; potentially a $3T deal with aid to the States and Municipalities. Republicans will likely want to stick with something like the $1.9T offer we saw earlier this month. Either one will help. The outcome of the election may impact the timeline for additional stimulus. Mixed scenarios, like a Biden win and a Republican Senate, or a Trump win and a Democratic Senate would add some twists, but I believe they will still result in a new package. The longer the process takes, the more nervous the markets will be. 2. Stock ValuationsMany of the stocks that have driven the indices higher are at extreme valuations by historical norms. No one says they can’t go higher, but it’s likely that there will be a reckoning, and some have a long way to fall before they’ll become a good buy. On the bright side, many individual stocks are offered at more reasonable valuations and may find some upside with stimulus and a solution to the health crisis. 3. Vaccine or CureNot much to say here other than when it happens it will be a good thing. We’ll be able to begin building our post-COVID economy and maybe find a new group of winning companies. This will be very helpful to “main street.”

Looking out past the above topics, we must address another collection of challenges, too long to go into much here, but I’ll list a few: All of that stimulus comes at the cost of massive debt. How we deal with this over the next decade will determine how we fare as a nation and as investors. It’s looking more and more like we are swallowing the Magic Pill of “Modern Monetary Theory” leaving little choice but to have faith inflation and interest rates will be tamed over time. This will impact our long-term growth prospects, potentially in a negative way. Taxes are likely to change; sooner if Mr. Biden is elected and the Senate falls to the Democrats this year. You can look up Biden’s thoughts on taxation on his campaign website. It mostly focuses on high earners, the wealthy, and corporations. This will change spending behaviors in unanticipated ways and is likely to slow growth to some degree. It’s also likely that all working Americans will see a tax increase in the future as we deal with the aftermath of additional debt generated by COVID and fiscal spending. Financial markets face many challenges, but we also believe that they present opportunities. For instance, as we mentioned in our most recent quarterly letter, valuation spreads between value to growth stocks, and small cap to large cap stocks has reached historic highs. So even with the broad markets being priced to perfection, investors that are willing to do their homework (like us) can find opportunities in companies and asset classes that have not participated to the extent as the “glamour” stocks have. Our disciplined process and focus on risk management will allow us to navigate the equity markets, no matter the victor of next week’s election. Humbly yours, the Cairn Team Greetings from the Northwest. Well, it’s Fall at last and it’s beginning to cool off a bit, although more slowly than usual, as it’s still been in the 80s when the smoke’s not too thick. We did kick off October with the first foggy mornings of the season and that seems to make a cup of coffee just a little more enjoyable. I look forward to the wonderful, natural changes that happen this time of the year, in stark contrast to some of our human constructs. Below, I’ll dig into some of my thoughts about our man-made world, but first I’ll share a moving personal experience with you. Some weeks ago, I woke up along the banks of the Madison River in Montana, having spent a few days fishing and revisiting one of the favorite memories from my youth. Wow, had it changed! Trophy homes are perched on every hill and a very active tourist/fishing racket drags paying customers down the river in small armadas, slapping the water continuously with their bright strands of fly line, all hoping to catch the same fish that had successfully ignored the prior dozens of presentations. Having had enough of that, I packed up camp early and headed east to Wyoming, through Yellowstone Park. I always enjoy Yellowstone, but unless one can stay awhile and explore, it’s just a slow drive through some pretty country, albeit a bit smoky this time. Midway through the drive, along the banks of the Yellowstone River, I found myself coming to a halt behind a line of stopped cars and a scene straight out of an apocalyptic movie, with drivers abandoning cars mid-road, grabbing cameras and optics, while lunging towards the river with much excitement. What I witnessed was one of nature’s greatest and most brutal spectacles. A very large grizzly had chased a mature bull elk into the river and was dispatching him as I arrived. Despite the elk’s long powerful legs and massive pointed antlers, he was no match for the bear’s practiced approach and agility. By entering the river, he had unwittingly sealed his fate. I watched as the bear finished this task, essential to his survival, and then slowly, working with the current, brought the elk to shore. Having assured survival for another week or so, he sat on his haunches, resting and considering his victory. This entire episode, from well before I arrived on the scene and for days thereafter, has been photographed and recorded by many, and you can easily find this on YouTube if you’re interested.  To the Victor Go the Spoils While this is a cool story and a great memory for me, I think it also has some instructional value when it comes to our lives, our decisions and our investing behavior. The outcome of this event was not preordained. Why did the elk give up its advantage and play into the strengths of the bear? My theory is that in this case the bear was much more experienced at killing than the elk was at not getting killed. The elk lived in a predator-rich environment, being on guard at all times and occasionally experiencing the loss of a herd member, but it probably had not been in such close proximity to death and had an exaggerated sense of his ability to escape. He was the amateur in this fight. Seeking safety was his undoing. By contrast, the bear, evidenced by his mere existence, was a professional. Each and every meal not scavenged, was preceded by a successful hunt. He is an expert at the end game. I draw a parallel from this to our own behavior: what we think and do when we’re afraid, and again when we’re confident. Our current human environment is unprecedented. To some extent we are all amateurs today. Who could imagine a year when the impeachment of the President of the United States is page three news? I cannot claim that we here at Cairn have some special insight into the future, or that we’re even smarter than the average bear, but I can tell you that we have a process and that process works much better than running into the river for safety. Please take a moment and consider what Patrick has to say about what we do and what we plan to do to keep your money in a good place. Patrick's PartIt was only a few short months ago that we were writing about the deep recession and corresponding market correction. Contrast that to today where we’re witnessing exuberance in parts of the equity markets that resembles the tech bubble that took place 20 years ago. The US stock market, not to mention Robinhood traders, must be fans of the late musician Prince because it is partying like it is 1999. My apologies if that song is now stuck in your head. The difference being, in 1999 you had stock tips on AOL message boards and discount brokerage firms that would take your trades 24 hours a day. Today, you have a slew of new traders with Twitter and a phone app that lets you trade stocks like a video game. We have written in previous quarters on some of the reasons investor enthusiasm is at its peak (Fed intervention, low interest rates, etc.). This optimistic behavior has driven valuation metrics across the board to historic highs. One of our favorite valuation metrics is the Price to Revenues (P/S) ratio. It gives a clear picture of what investors are willing to pay for a stream of revenues before costs and other accounting factors. It has been observed that there are now more companies in the S&P 500 trading at 10 times revenues (37) than there were in March of 2000 (30). This data point reminds me of a quote from former Sun Microsystems Founder and CEO, Scott McNeely, when he discussed the investor euphoria that was taking place prior to the tech bubble bursting:

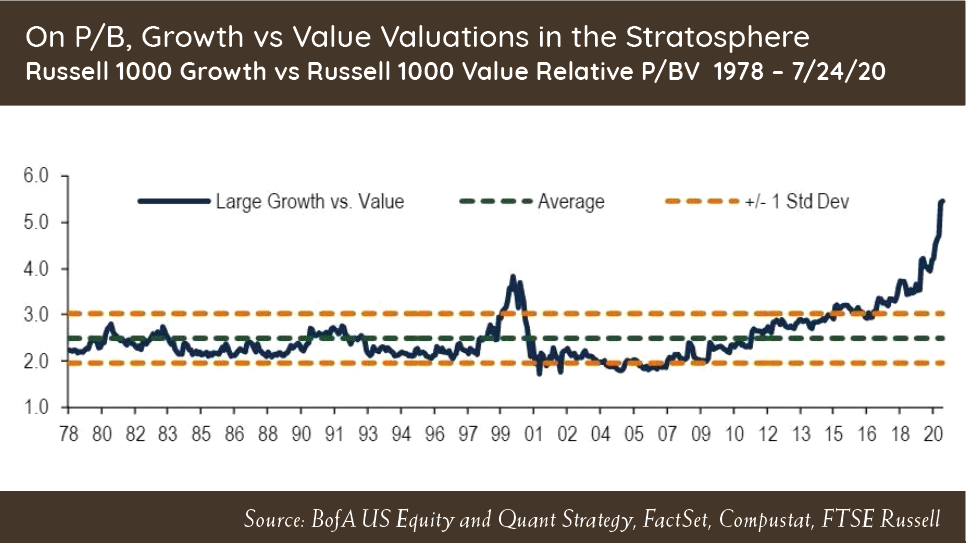

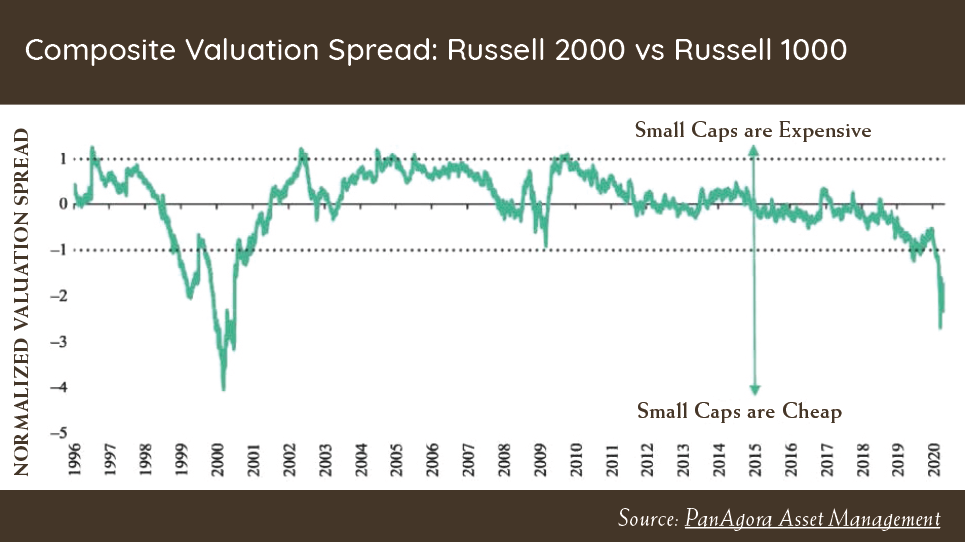

The recent price performance of Tesla showcases a current example of investor euphoria when their share rose 50% after the company announced a stock split on August 11th. A stock being split may sound like a good thing, but there is no economic value created with a stock split! The market value, earnings, revenues, and cash flows of the company remain the same. There are simply more shares outstanding being offset by a lower price. Tesla’s 50% increase in market cap in the two short weeks following their split announcement generated more wealth for investors during that period of time than any of their car designs have ever done. Wonderful companies (many of which we own) that create essential products and services have seen their share prices shoot past the fair value of the underlying business. However, this means that the prospects of these companies have been accounted for in the high share price. This potentially leaves little room for growth and heightens risks if the prospects fail to materialize. Down the road many investors may be looking back on this period asking themselves, “What was I thinking?” With the levitation in growth stocks, investors have ignored other well-run businesses and asset classes. This is where we are finding opportunities for new investments. As value investors, our primary focus is not looking for new investments based on what has previously done well, but rather we look for companies and markets that are under appreciated that will do well in the future. The current divergence in price returns has been shown to reward some companies too much while punishing others too harshly. Mean reversion is a powerful phenomenon and the evidence suggests that such anomalies tend to reverse. Below are charts showing the relative valuation of value stocks vs growth stocks, and small company stocks vs large company stocks.   Looking at these charts together tells a strong message. While focusing on risk, the opportunity for investors to earn returns is found by looking at value over growth and smaller companies over larger companies. The companies and asset classes we are investing in fit this criterion as investor enthusiasm has swung the pendulum to extreme levels in both instances. Unfortunately, no one can predict precisely when the pendulum will lose momentum and swing back in the other direction. We continue to focus on what we can control: being disciplined, patient, having a historical perspective, and straying away from the herd when opportunities or excessive risks are present. Thank you for your continued trust and please reach out if you would like to discuss any topic in greater detail. Stay safe and healthy.

Thanks, Patrick.

Wishing you all good health and dry feet as the Autumn soaks in. Happy trails, Tim Mosier, President Cairn Investment Group, Inc.

Greetings,

Just a quick late summer note to keep you up to date with some of our thoughts and observations. While some of you are off fighting wildfires, watering lawns and gardens, or hanging out at the beach, we’ve stayed put through this summer of the virus, making investment changes as we see opportunity or risk. The stock market has rallied off of the March lows and is now officially in a new bull market, with the S&P 500 having hit a new all-time high. This has been the fastest recovery in history following such a decline; following the fastest drop ever from an all-time high into a bear market. That said, this has not been a broad market rally, with multiple sectors still languishing just a few percentage points above their lows. These are generally businesses awaiting word on when the COVID recession will end, triggering increased product demand and a clearer path to safety. Financials, Retail, Energy, Real Estate and Utilities, often stalwarts of the economy (and great dividend payers) are either in bear market terrain or are noticeably lagging the indexes. The driving force behind the new records has been primarily big tech; not just any tech, but BIG tech. These firms (Microsoft, Apple, Alphabet, Amazon, and Facebook), represent only 1% of the S&P 500 by count, but about 25% by value; and this increases as they continue to get media and buyer’s attention. This is the largest bias towards outsized firms ever. It’s understandable with current circumstances that all five of these giants have and will continue to reap outsized rewards due to our dependence on e-communication and e-commerce. We could not run Cairn without the products that Microsoft and Apple provide. That being said, it’s quite possible that (some of) these leaders are too far ahead for their own good, as momentum can push the markets far past fundamental support. Traditional value metrics are beyond stretched, investor behavior indicators are flashing warning signs that should be noticed, and at this point greed should be taking a back seat to caution as we have more months of recession ahead. Another, less publicized area of risk is in the bond markets, particularly with low to medium quality corporate debt. Defaults are rising, and this probably will continue for some time into the future. In some parts of the country municipal bonds pose a risk. I think that we’re well positioned here, with very little exposure to at risk debt. Our Oregon munis are primarily covered by property taxes and have so far proven to be resilient. We’ve taken all of this under consideration while making our investment choices and will continue to do so. If you have a desire to discuss any of this, or any other concerns that you may have, please give us a call, and either Patrick or I will be happy to have that chat. Here’s to a few more weeks of sun and then a glorious fall. Your Cairn Team Greetings from the Northwest. Or should I say… Sweden? After all of the care we took to contain the virus and after all of the disruption to our lives, businesses and, yes, investments, we apparently will be moving forward by adapting and learning to live with the killer. While our bodies are no better prepared to fight the virus than they were in February, the medical and political systems have had time to react and strengthen their responses. We now have masks aplenty, and, apparently, an adequate number of ventilators. There’s been a noticeable lack of noise lately about vaccines and treatments, but I trust that, quietly and efficiently, the medical community is honing their response. Human nature is revealing itself, in that people are bursting their seams to get out of the house and back to work, school, play or protest, and so it shall be. So, what does this have to do with investing? Everything, I say! It has everything to do with how vibrant the economy will be, who the winners and losers will be, and how much confidence, or lack thereof, will be floating the stock market. As I write this, the market indices are again near their historic highs. Does this indicate a ground swell of confidence, or opportunistic speculation that the Fed will keep injecting funds into the system? It’s probably a little of the former and a lot of the latter. Life and the economy are always complex, with forces coming from many directions, some opposing, some reinforcing, some just confusing; but in our lives this is probably one of the most complex. With the headlines focused on major social and health issues, it’s easy to forget that many millions of hard working people are out there every day, trying to make a living and better their situation. Rush hour traffic is packed with folk headed to work. Heads down, full steam ahead. It’s this that makes what we do possible. There is no upside to the stock market or juicy dividend payouts without it. We hope and have confidence that this will always be so. While the market indices are at high points and their measurable valuations are near extremes, many investable securities have not participated fully, and we are finding a few opportunities. Keeping cash and fixed income productive is a challenge as well, with yields being extremely low. I’ll let Patrick dive a little deeper into what’s dragging the markets around. A Quick Office UpdateWe’re still closing early at 4pm each day, with Patricia and me onsite. Patrick and Jesyca join us each Tuesday so we can push forward on a number of projects we’ve undertaken. Jim and Lara check in multiple times a week and have lately been in at mid-week. Speaking of projects, the most important is our conversion from Envestnet’s “Portfolio Center” to their more advanced “Tamarac” reporting system. Your quarterly report, attached, looks very different from what we’ve produced in the past, and we believe this will enable an enhanced understanding of your investments. We look forward to your feedback. Another improvement is the ability of this system to open a private client portal to securely deliver documents, and to allow you to view your investment progress at your convenience. Our plan is to begin distributing Quarterly Reports through this secure client portal in October.  Photo by Liesl M.

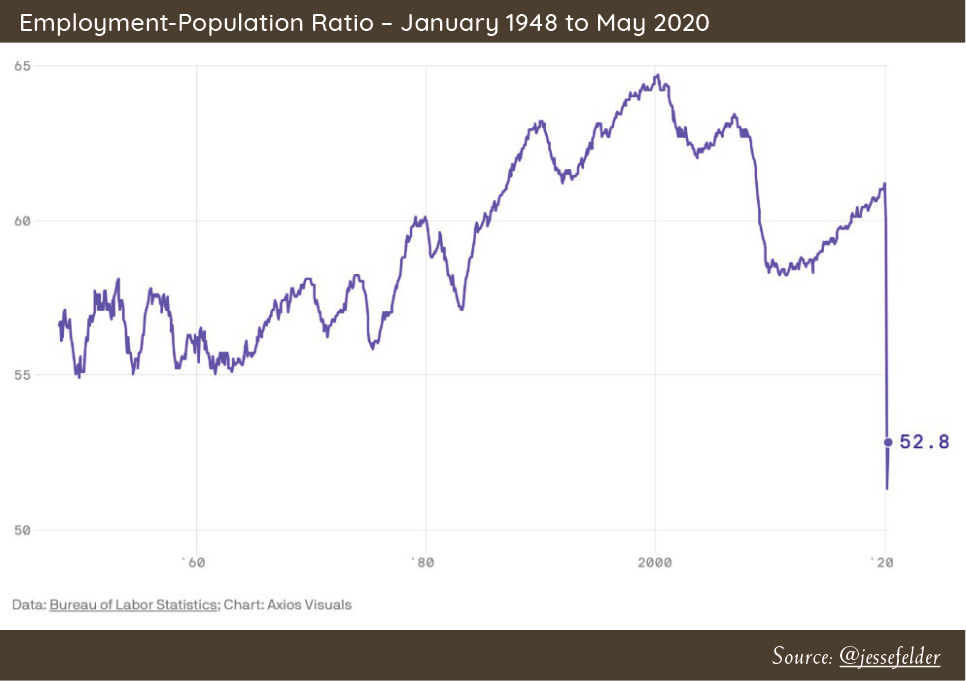

Patrick's PartThese are truly unique times we are experiencing. The volatility of equity markets so far this year is something that has not been seen since the Great Depression. In the last 3 months, global equity markets went from fear of an economic collapse to trading at the same lofty valuation levels that were seen in January, before the pandemic took hold. On June 8, the National Bureau of Economic Research officially declared the US to be in a recession that had started in February. It seems like with the recent surge in stocks, markets have priced in a swift V-shaped recovery in economic growth and corporate earnings. We are not going to pretend to know how this will play out. However, we find the view of a return to economic and earnings prosperity in the near term to be Pollyannaish, as the majority of “Main Street” are still suffering from lost jobs and lack of consumer confidence in the safety of going out and living a normal life without getting sick. The Fed is a primary catalyst to the stock market’s newfound enthusiasm. On March 23, Fed Chairman Jerome Powell announced unprecedented (some would argue illegal) financial liquidity to the fixed income markets. Never before has the Fed embarked on directly buying individual corporate bonds. In our opinion, this direct backing of individual company debt is blurring the lines of free markets and creating a large moral hazard in corporate America. The Fed is now a top 5 holder of the 54 billion-dollar iShares iBoxx Investment Grade Corporate Bond ETF that holds individual bonds issued by companies such as Microsoft, GE, Anheuser-Busch, Berkshire Hathaway, and CVS Health. This means the Fed is now investing in and supporting individual company debt, having the potential ramification of choosing which type of company could succeed and fail, instead of the capital markets making that determination. The backing the Fed has provided to the bond market has spilled over to the equity markets in the hope that monetary intervention will be the panacea for the current downturn in company profits. The chart below from Charles Schwab Chief Strategist, Liz Ann Sonders, shows the growth in the Fed’s balance sheet and the price of the S&P 500 index. The Fed’s intervention corresponded with stocks moving higher:  Meanwhile in the real economy close to 50% of the population is not working:  Many market pundits argue that the stock market is not the economy and that stock markets can look forward to an eventual economic and earnings recovery. This is true, but significant price recovery usually takes place when market valuations are much lower than where they currently stand, at close to 30 times normalized earnings.  It is not hard to argue that the disconnect between stock prices and the real economy is quite large. Our job is recognizing the environment we are investing in, managing risk, and finding opportunities. On May 11 we sent out our mid-quarter update, discussing where we are finding opportunities, and said:

Our thoughts have remained the same and we continue to find opportunities that fit that criteria. We would not be surprised to see continued volatility in financial markets, as states react to the virus and open and close communities accordingly. We will continue to act prudently and manage your wealth based on data and analysis, not on headlines and emotions. Thank you again for your continued trust, and please feel free to reach out to me to discuss any topic in greater detail.

Wishing you health, happiness, safety, and enjoyment as we head into another Pacific Northwest summer. Tim Mosier, President Cairn Investment Group, Inc.  Greetings, It's Patrick here following up on Tim’s post from last week, explaining in more detail how we view the current investment landscape. From an economic perspective, the slowdown in activity has been nothing like any of us have seen during our lifetimes. The contraction and number of job losses was last witnessed during the great depression. Reading through various reports makes you realize how traumatizing the virus has been to most Americans. If one just looked at the S&P 500, you would think that everything is the old status quo and that we had just a minor correction. The disconnect between what “main street” is going through and what the stock market is going through is a head scratcher to say the least. I wrote about valuations and bear market experiences in our last quarterly letter so I will not spend a lot of time rehashing the topic again, except to say large cap U.S. stocks are still trading at lofty valuations and that the current market experience we see is still typical of historical bear market experiences. We will change our view when the data warrants it, but for the time being caution is still a primary objective. The silver lining to this environment is that there are pockets of the market that have had a worse experience than the S&P 500, and that is where we are finding opportunity to put cash to work. For instance, small cap stocks (companies that have a lower market capitalization) are trading at valuation discounts that we have not seen in over 20 years. When analyzing the data, other periods of such wide divergence have generally led to higher returns for small cap equities over large cap. Many of the individual companies we invest in have much smaller market caps than the S&P 500, so this should benefit the portfolio going forward. Additionally, select industrial, consumer discretionary, technology, and health care names have experienced much larger declines during the recent market selloff, creating some opportunities for investors that do their homework (like us). Tim touched on the absolute outperformance of the technology sector versus the rest of the market. The companies that have benefited most from employees having to work from home have seen their share prices levitated to truly astounding levels. Looking at the last time we saw this level of outperformance we can see the narrative is similar between our current environment and the one back in 1999. The story was, “Technology and the internet are going to change the world forever, so revenue growth is all that matters.” Which was true, but it did not stop large tech from losing over 70% of its value. Now the narrative is “Tech companies can weather this recession because of workers staying from home and their capital requirements are low.” This is also true, but the price investors are willing to pay for future growth of these companies seems to be excessive here (chart below).  Source: Bespoke Though the economy is most likely going to get worse before it gets better, we as investors, must look through the noise and use a historical perspective when looking for opportunities. There are areas of the markets that offer compelling risk/reward tradeoffs and we are taking advantage of them. However, the data does not indicate that portfolio positioning should be tilted towards maximum risk. Still holding a higher amount of safe assets (cash, T-Bills, etc.) makes sense until broader valuations improve. Thank you again for your continued support during this trying time in our economy.

Please drop me a note if you care to discuss anything in greater detail. Best regards, The Cairn Team Greetings,

It’s been a month since our Quarterly Newsletter went out, and I thought that you might appreciate an update on our office situation and some thoughts on the COVID economy. Our office remains closed to visitors, and I expect this to continue through the end of May, probably longer. We are getting reasonably adept at online meetings through WebEx, so if you feel the need for a catchup discussion that requires more than a phone call, please, let us know and we’ll set something up. Patricia continues to report into the office every day, handling incoming calls, deliveries, and various office tasks. I’m here 2 to 4 days a week, trying to reduce my chances of getting infected, but remaining otherwise effective. The rest of the team works remotely. Remote work is interesting, and I think very different than most of us imagined. The ability to make a call, trade securities, do research, etc. is essentially as good as it always was. There are some challenges with reviewing items by multiple team members; all surmountable. The real difference is the lack of easy, casual interactions that help stimulate thoughts and redirect energy. I’ve likened this to “dancing without music.” There is nothing stopping one from taking the first step, but conversely, nothing provides a cue to start either. It takes some getting used to. Equity markets are up considerably since the last time I wrote. I can’t say that this offends me in any way, but it does seem a bit optimistic as most of the bad news in the form of poor quarterly earnings, dividend reductions, companies pulling guidance, high unemployment, and a GDP reading indicating a deep recession has not yet been heard. At this point much remains to be known, as most indications signal that the shutdown will reverberate for quite a while into the future. A big bright spot has been technology stocks, which, as a group, are up for the year. This reflects a number of factors, not the least being our obvious dependence on technology to get through times like this. It does make one wonder ultimately where this goes; how much further can they go up without having their own 21st century tech bubble. Overall, valuation is still a concern, as US large cap stocks are close to levels seen only a few short months ago. I’ve asked Patrick to discuss this in a separate post that you’ll see soon. He’ll detail our thoughts on what to expect and what we are doing as we go through this exceptional Spring. Until we meet again, I wish you and yours well. The Cairn Team Greetings from the Northwest. In this unprecedented, historic, and frightening framework I struggled with writing that simple, well-used phrase. Is it too light and cheery for the circumstances we find ourselves in? Will this arrive at a home stricken by the virus? I can’t know, but I sincerely hope that this finds you and your loved ones healthy, and happy to be enjoying more time together at home. This is such an exceptional time. We’re all in the same boat, and that phrase works so well here, yet the way it plays out for each of us will be unique. I have few worries for myself, but my paramedic daughter is deployed with FEMA at a hot spot, and I worry for her every day. My son is currently submerged somewhere in the Pacific on board a submarine, and I last heard from him in late January. Does he even know about what’s happening? Many of you have stories and concerns of your own, I’m sure. Dealing with the health and safety is and should be the overarching priority. Through all of this, Cairn’s job is to care for your money, and give you confidence that this will work out for you financially. We’re all fine here, and we are functional. We are adapting. I write this sitting in an otherwise empty office, just having gotten off a teleconference with the staff, most of whom are working from home. For the first time ever, this newsletter and attached reports are being generated and distributed electronically. Patrick has all of his Cairn tools at home, as does Jesyca. Patricia works her normal shift in the office, fielding the incoming calls and mail. Jim and Lara remain ready to help at the push of a button, so rest assured that we are here, and will be here through it all.  Patricia, Holding Down the Fort at Cairn HQ Investments have taken a hit. Considering the backdrop and the potential economic harm that’s being inflicted, it’s heartening to see that it’s not been worse. This might be a recognition that all stops will be pulled out to get the nation through this. I do think that more rough times are ahead, but at this point we are beginning to look for opportunities as much as we are looking to reduce risk. Patrick will go into details about the process and economics, but I will say here that if you have enough cash and fixed income to support your plans for the next year or so, it’s likely that your equities will have recovered nicely by the time you’ll need to tap into them. Let us work the process and position things for the eventual rebound. I’ll end with a quote from Warren Buffet that Jim shared with me recently: “The stock market is a device for transferring money from the impatient to the patient.” We are patient. On to Patrick…

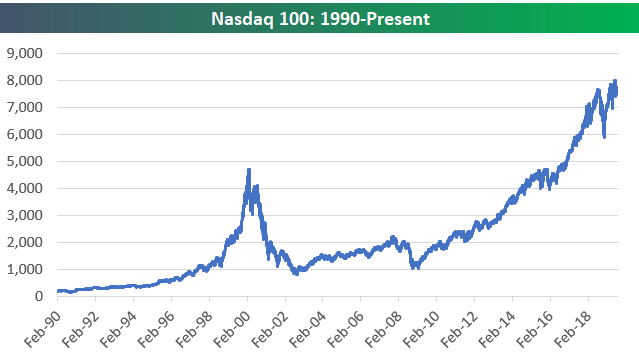

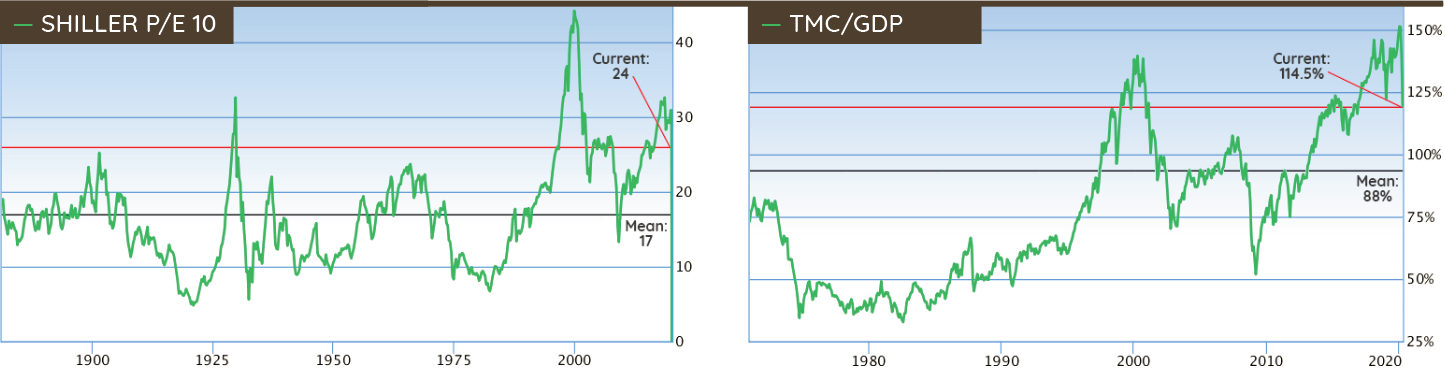

Patrick's Part It’s hard to believe that most stocks were trading at a record high only 6 weeks ago. The rate of this recent downturn was the fastest in history. US large cap stocks fared the best, being down 19.6%. US small cap stocks, developed international stocks, and emerging market stocks were down more, with returns of -30.65%, -23.01%, and -23.94% respectively. The bond market was also quite volatile during the quarter, with the broad market returning 3.10%, high yield bonds down -11.61%, and municipal bonds returning -0.61%. Needless to say, outside of cash and Treasury bonds, there were few safe havens. The response to COVID-19 has inflicted significant damage on the global economy to date, with little clarity on when the economic data will start to take a turn for the better. We have talked in great length in previous letters regarding our thoughts on the economy, high market valuations (Oct 7 2017 :: Jan 11 2019 :: Oct 8 2019), and interest rates (April 12 2019), but I don’t think anyone could have foreseen the rapid impact this virus is having. The US is most likely in recession at this point, which prompts the questions: How long will this contraction last, and what impact on consumer behavior and spending will it have on the rate of recovery? Unfortunately, nobody knows the answers to these questions. Recently, we’ve communicated how we are managing the portfolios during this difficult environment and our process for uncovering new opportunities (July 11 2019), so I won’t spend a lot of time on that here. My focus is primarily on the broader US market and where we stand from a valuation perspective after the recent price declines. For comparison we will look at price behavior during a recent bear market. With lots of noise in the short-term, I find it helpful to focus on a long-term perspective to provide some clarity on expectations of future market returns and experiences. The prevailing viewpoint amongst market pundits since the last week of March is that the low was reached on March 23rd when the S&P 500 closed at 2,237.40. This combined with the narrative that prices will be choppy, but higher prices are to be expected in short order. It’s a nice story and feels good to hear that the worst could be behind us. And (while it is possible that the pundits are correct) after examining the data and comparing previous bear market experiences, it could prove to be wishful thinking. We do not invest on hopes and wishful thinking, though, and prefer to look at hard data instead. The charts below show two different metrics that are very useful in understanding long-term valuations. I have discussed these previously and reviewed them with many of you individually.  Source: GuruFocus

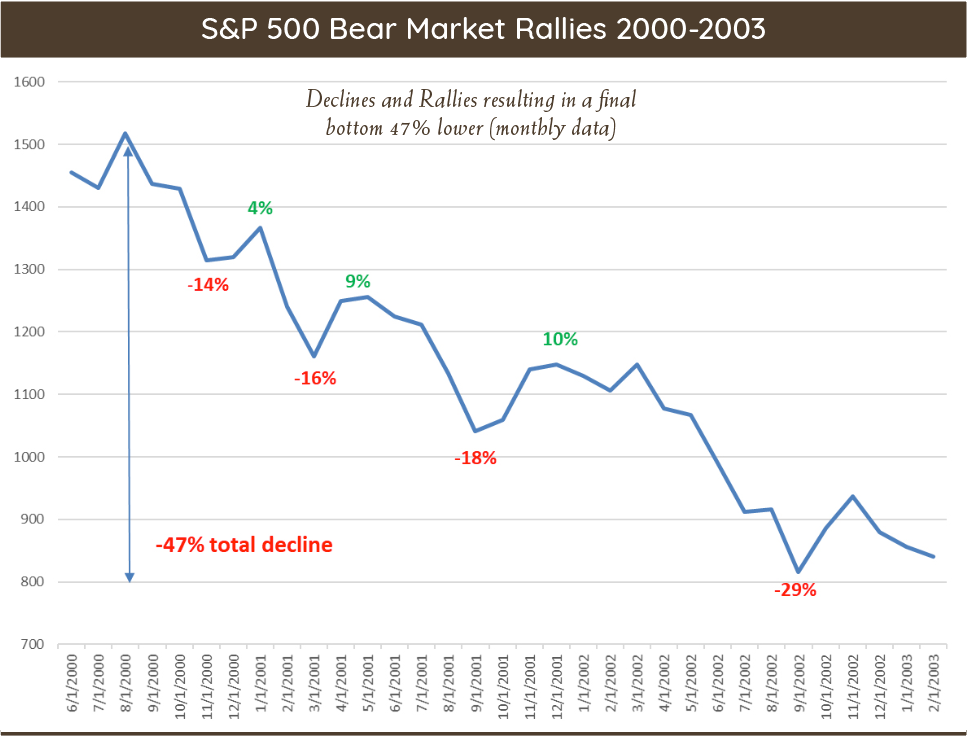

The Shiller CAPE P/E ratio and Total Market cap to GDP both peaked at the end of January. As the charts show, both indicators are down from their highs set earlier in the year. However, even with the recent improvement in valuations, these metrics are still only 20% below levels that were matched only during the Great Depression and the tech wreck. I don’t bring this up to say the market has to head lower, as investing is not an exercise in absolutes, but to give context to where current valuations stand versus history. Even after recent price decline, valuations are still elevated. The month of March was extremely volatile. Not since the Great Depression have equity markets seen this level of volatility. From March 1st to March 23rd the S&P 500 was down 24.16%. Then from March 23rd to March 31st the S&P 500 rallied 17.4%. The rally from March 23rd has caused many pundits to declare that the “bottom” has been set and the next bull market is underway. Nobody knows when the bottom happens. It is only known well after the fact when prices are higher over the long-term. The chart below shows the price experience of the S&P 500 during the bear market that took place from 2000-2003.  As the chart shows, the decline that took place was filled with many short-term rallies that ultimately failed as prices moved lower. Again, this is not to say that the current market behavior will mirror the above experience, but to give a longer-term perspective on how markets can behave. They do not continuously go down during bear markets, nor do they continuously rise. We follow price trend data very closely as part of our analysis and the data still suggests a new bull market hasn’t begun. The combination of valuations and price trends leads us to believe that caution is still warranted at the broader market level. However, during bear market environments there are individual stocks, sectors and asset classes that perform much better than broad indices. On a positive note, with the recent market decline, we are starting to find many more suitable investments that didn’t exist a few months back. Many stocks have seen declines of 30-50% this year, compared to 20% for the S&P500. This is creating opportunities and we are taking advantage as prices dictate. During this period of stress, we continue to emphasize attractively valued companies, with durable cash flows and strong balance sheets that can weather this economic storm. We will continue to invest based on our disciplined process, and let facts and data tell us when we should change our mind on when taking more risk is necessary. Thank you again for your continued trust and especially your kind words during these trying times. Please drop me an email or phone call if you want to discuss any topic in greater detail. Thanks, Patrick. With that I’ll leave you all with the sincere hope that you remain safe through this perilous time. Tim Mosier, President Cairn Investment Group, Inc.  |

RSS Feed

RSS Feed