|

Greetings from the Northwest. I love this time of the year, and I know many of you do too. The welcome relief from the heat, with a cool fresh breeze, soaking rain and magical, mystical fog coming to the rescue of flora baked and broiled through this hot dry summer. Trees turn brilliant colors, salmon leap at the falls, waterfowl get ready for their annual migrations; here and there someone lights a fire in their hearth and shares a warm drink with a friend. All is wonderful, and for now, new and exciting. It’s fall. On many counts it’s another normal fall. Kids are in school, the stock market is getting choppy, and politicians are back at work doing whatever politicians do. I do hope they choose to continue funding the government. There is that COVID thing, though. I don’t think that last year I thought I’d still be asked to wear a mask at this point, but unfortunately here we are. Whether it’s exhaustion or unwillingness to continue with extreme shutdown measures, or wisdom gained through hard-won experience, we do seem to be weathering this better economically than we did last year, despite the surging infection rates. There are some economic oddities that we can blame on the pandemic, and one that many of you are experiencing is related to a damaged global supply chain. Try buying new furniture or finding a replacement part for your car. You might be waiting weeks if not months. Aside from the obvious inconvenience and irritation this may cause, it’s also a symptom of supply and demand that are out of sync; probably and hopefully temporarily, since this was caused by a shock event. However, we all know that more demand than supply leads to higher prices. Patrick will again dice and slice this in his section, with some new and intriguing angles.  Photo credit: T. Mosier, Pershing, Nevada

Another, not unrelated, economic oddity we’re experiencing is the surge in home prices, not just in the predictable core urban areas, but in the far suburbs or “exurbs” as people seek a bit more space between themselves and others or flee urban crime and blight. Freed for now from commuting constraints, high-paid professionals are even driving up prices in cities far from their employers; Bozeman, Montana comes to mind. With that I’ll hand things over to Patrick: Patrick's PartFinancial markets showed more volatility during the third quarter. Large cap stocks were the best performers, rising a modest 0.58%, driven by the biggest cap stocks. Peeling back the skin, performance of equities showed mixed results with large value stocks declining -0.78%, small cap stocks returning -4.36%, and international stocks returning –0.45%. Bonds did their job, showing low volatility and modest returns of 0.05%. In the past two quarters we have written about the effects of inflation on equity markets, the current high valuations of large cap stocks, and how we would manage through a period of higher inflation. In recent months the hard data surrounding inflation, and the commentary from company management, have made it clear that inflation is here, and how quickly it will subside is anyone’s guess. Though The Fed has been adamant that inflation will be transitory due to the pandemic, in their September policy meeting they admitted that inflation has lasted longer at a higher rate than anticipated. I indicated last quarter that the bond market has not been a believer in the inflation narrative. However, the bond market can only turn a blind eye for so long. The prolonged inflation picture could have effects on the following: consumer behavior, how profitable companies will be going forward, and how the equity markets will behave. First, on the effects of consumer behavior. Here is just one example of the headlines investors and consumers were reading from the Wall Street Journal on September 26th:

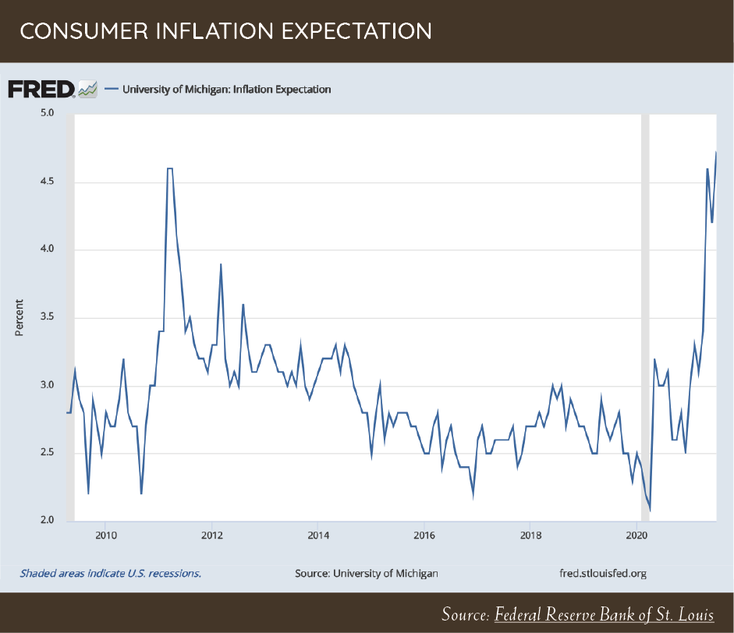

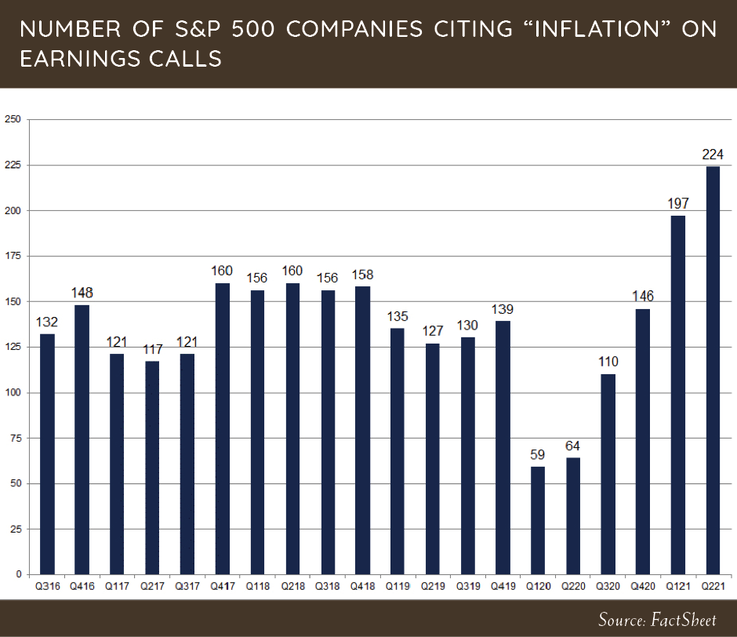

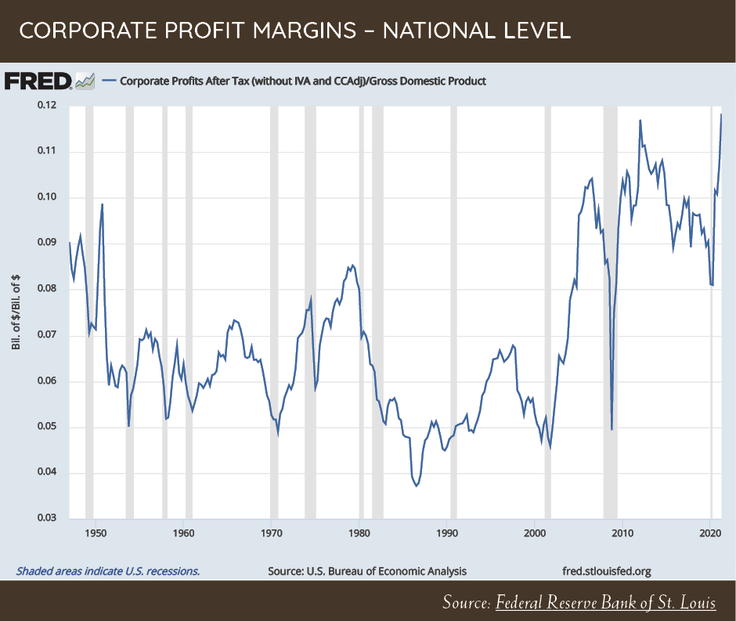

I have discussed the inflation topic with many of you over the last 12 months, and one thing I have said is that inflation can take hold because people believe it will take hold, like a self-fulfilling prophecy. As demand for goods continues to be high, while supply of goods is low due to supply chain issues, consumer behavior could change based on the expectation of higher prices, causing the very thing that everyone fears the most, inflation. The chart below is a survey measuring inflation expectations from consumers. As you can see, it is the highest since 2011.  Inflation’s effect on corporate profit margins will be highly dependent on a company’s ability to pass higher input costs to the end consumers. In our analysis of each company we own, we stress test their cash flows, considering negative effects of inflation and profitability when we determine a fair value. One thing is for sure: company executives are talking about inflation. Below is a chart showing the number of S&P 500 companies that are mentioning inflation in their earnings calls.  With nearly 50% of companies mentioning inflation in earnings calls, there seems to be a real concern about inflation amongst companies. Executives are going to have to make some tough decisions about how to allocate capital going forward if costs continue to rise and profits start to come under pressure. This is one of the many reasons why being disciplined in the price you are willing to pay for a company is so important. Paying too high a price during a period of eroding profits is a dangerous recipe. Over the last few quarters, we have talked about what the effects of inflation would be on equity markets, so I will be brief. The chart below shows corporate profit margins at a national level. As you can see, profit margins are at an all-time high.  The combination of record high equity valuations with record high profit margins could prove to be a challenge for equity market performance if inflation starts to erode profits. Though we view many large cap stocks as being expensive, we are still finding opportunities in select individual companies and certain asset classes. Over the last year, portfolios have been rewarded by having a value and small cap bias. The main detractor to performance has been our allocation to emerging market equities. Though the underperformance of emerging market equities has been disappointing, we believe we will be rewarded in the long term as valuations are much more attractive compared to the United States. Our portfolios continue to have a conservative bias and hold slightly more cash than normal, due to the risks that are present in equities combined with the low opportunity set available. Thank you for your continued trust and support. The topic of inflation and the effects it will have on capital markets is complex, so feel free to reach out to me with any question. —Patrick Mason

Thank you, Patrick. We’re all curious to see how this plays out.

Goodbye for now and Happy Trails, Tim Mosier, President Cairn Investment Group, Inc. Comments are closed.

|

RSS Feed

RSS Feed